Off-payroll working (IR35) – calculation of PAYE liability in cases of non-compliance

Updated 22 November 2023

© Crown copyright 2023

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: [email protected].

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/consultations/off-payroll-working-calculation-of-paye-liability-in-cases-of-non-compliance/2a24e825-3ca0-44f5-9862-6d794da72bda

Summary

Subject of this consultation

A consultation on a possible change to allow HM Revenue and Customs (HMRC) to account for taxes already paid by an individual and/or their intermediary when calculating a Pay As You Earn (PAYE) liability due by a deemed employer where an error has been made in applying the off-payroll working rules.

Scope of this consultation

The purpose of this consultation is to set out a potential option for a policy to address this issue and seek to ensure the option works effectively and understand how this would impact different parties in the labour supply chain.

This consultation seeks views on the policy before deciding on the best way to address the issue.

This consultation is not seeking views on changes to the off-payroll working legislation more generally or how employment status is determined.

Who should read this

People who work through their own intermediary (for example, a personal service company (PSC)). Medium and large-sized clients, public authorities, agencies, partnerships and individuals who engage people who work through their own intermediaries. Accountants and other agents representing people who work through intermediaries or representing engagers of people working through intermediaries. HR managers and those who deal with recruitment processes and payroll.

Duration

The consultation will run for 8 weeks from 27 April 2023 to 22 June 2023.

Lead official

The lead official is P Staton of HMRC.

How to respond or enquire about this consultation

Please send email responses to [email protected] or by post to:

Off-Payroll Working Policy

3E/4

100 Parliament Street

Westminster

SW1A 2BQ

Additional ways to be involved

HMRC will work with representative bodies to arrange events where there is sufficient interest.

After the consultation

The consultation will inform decision-making on how best to address the current issue. A summary of responses will be published later in the year.

Getting to this stage

HMRC has engaged with industry and representative bodies on this issue since 2021. Officials have held a number of policy development workshops with these stakeholders that has resulted in the identification of a potential option to address the issue, which is now being consulted on.

Previous engagement

HMRC officials held a number of policy development workshops with industry and representative bodies during 2022 and 2023. This issue has also been raised by the National Audit Office (NAO) and the Public Accounts Committee (PAC) in reports published in early 2022.

1. Executive summary

The off-payroll working rules (commonly known as IR35) were first introduced in 2000. The rules set out that where an individual is working like an employee, they should pay tax like an employee – regardless of whether they are working through their own intermediary (for example, a PSC).

The rules aim to ensure fairness within the tax system by addressing the issue of people working like employees but through an intermediary simply to avoid paying employment taxes.

When the rules were introduced, it was for the worker’s intermediary to decide whether they were working like an employee, and therefore in scope of the rules. However, there was increasing and widespread non-compliance with these rules.

Consequently, the government introduced an administrative reform to improve compliance with the existing rules. The reforms were introduced for clients in the public sector in 2017, and extended to include medium and large-sized clients in the private and voluntary sectors in 2021. The reforms shift responsibility for determining employment status, and for ensuring the right tax and National Insurance is paid to HMRC, from the worker’s intermediary to the client engaging them.

If the client is found by HMRC to have made errors in determining the employment status of its off-payroll workers, the deemed employer (which could be the client or an agency further down the labour supply chain) becomes liable for Income Tax and National Insurance contributions (NICs) that should have been deducted from the fee paid to the off-payroll worker had the correct status determination been made. In this situation, HMRC may end up collecting more tax than is due because the worker and their intermediary may have already paid tax and NICs on the same income in the belief that they were outside the rules. The issue has been raised by stakeholders and highlighted by the National Audit Office and Public Accounts Committee, who published reports in early 2022.

Current legislation does not allow HMRC to set off amounts of tax and NICs already paid by a worker and their intermediary against the PAYE liability of the deemed employer. Instead, where a worker and their intermediary have paid tax and NICs on income that should have been subject to the off-payroll working rules, they may be entitled to claim a repayment for amounts they have overpaid. HMRC has implemented a process within its existing powers to notify workers and their intermediaries that they may be due a refund for taxes already paid on the engagement, where contact information is available.

The current process results in the deemed employer bearing the full cost of the tax and NICs liability. This consultation sets out HMRC’s considerations for, and invites views on, a potential alternative solution. This would introduce new legislation to share the Income Tax and NICs liability between the client and the worker, by estimating a set-off for tax and NICs already paid by the worker and their intermediary. These views will inform future decisions on the best way to address this issue.

2. Introduction

Where the off-payroll working rules apply, the deemed employer (which could be the client or an agency further down the labour supply chain) must operate PAYE on the payment for the worker’s services – meaning that they must deduct and pay to HMRC the relevant Income Tax and employee NICs, and pay employer NICs and the Apprenticeship Levy (if applicable).

If the off-payroll working rules do not apply, the payment is made without any deduction for tax or NICs. Instead, the income would be subject to Corporation Tax as part of the PSC’s business profits and the worker would be subject to Income Tax and NICs on any salary received from the PSC and tax on any dividends from the PSC.

When errors occur

HMRC may undertake a compliance check into a client to see if the off-payroll working rules have been operated correctly on their engagements. Sometimes, a client will contact HMRC to voluntarily disclose that they have made an error in applying the rules.

If it is found that the engagement was incorrectly determined to be outside the off-payroll working rules, the deemed employer will become liable to Income Tax and NICs that should have been deducted under PAYE, had the correct determination originally been made. Where the worker should have been inside the off-payroll working rules, the deemed employer is required to pay the Income Tax and NICs liability in full under the current off-payroll working and PAYE legislation.

In this situation, the worker and their intermediary would have thought their engagement was outside the off-payroll working rules. If the error is discovered after the worker and their intermediary have filed their Income Tax Self Assessment return and Company Tax return for that tax year, they may have already paid some Corporation Tax, Income Tax and/or NICs on that income.

This may result in HMRC collecting too much tax and NICs on the off-payroll working income overall. Under current legislation, the worker and their intermediary would be entitled to claim a repayment for any tax they have overpaid in relation to this income, subject to time limits and conditions.

If the error is discovered and corrected before the worker and their intermediary have filed their tax returns, there would be no overcollection of tax and NICs. Instead, the worker and their intermediary would need to file their tax returns on the basis that the engagement was inside the off-payroll working rules.

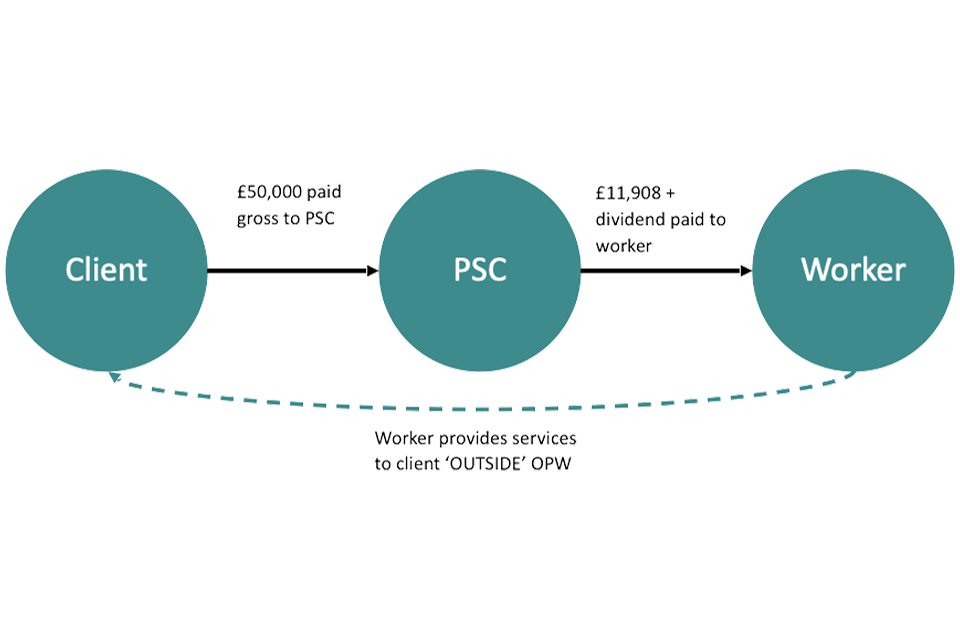

Illustrative example of the issue

Note: £11,908 is the Class 1 NICs annual primary threshold 2022 to 2023

In the above diagram, a client engages a worker through their PSC, to provide services to them, and agrees to pay a fee of £50,000 for these services. The client has assessed the worker as outside the off-payroll working rules and therefore pays the gross fee of £50,000 to the PSC. The PSC then pays the worker in the most tax efficient way, being a salary up to the Class 1 NICs primary threshold and the rest as a dividend.

At this point, the client has not accounted for any PAYE liabilities as they have determined that the engagement is outside the off-payroll working rules. The PSC will pay Corporation Tax on their business profits and the worker will pay income tax on their dividends. A small amount of employer NICs will also be due. For simplicity, we have assumed that there are no business expenses in relation to the engagement.

The tax position is therefore:

| Type | Corporation Tax | Income Tax | Employee NICs | Employer NICs | Total |

|---|---|---|---|---|---|

| Client | – | – | – | – | – |

| PSC | 7,160 | – | – | 404 | 7,564 |

| Worker | – | 2,439 | – | – | 2,439 |

| Total | 7,160 | 2,439 | – | 404 | 10,003 |

Note: This is calculated using 2022 to 2023 tax rates, thresholds and allowances

Later on, HMRC carries out a compliance check into the client’s determination and concludes that the determination is incorrect, and the engagement should have been inside the off-payroll working rules.

This means that the engagement should have been determined as ‘employed’ for tax purposes, and the payment treated as employment income of the worker. The client should therefore have operated PAYE on the £50,000 payment and paid the net amount to the PSC.

Therefore, the client is the deemed employer and is liable for the Income Tax and NICs that should have been paid under PAYE. In this instance, the liability is calculated on the assumption that the worker’s personal allowance has already been exhausted by other income, giving the following tax position:

| Type | Corporation Tax | Income Tax | Employee NICs | Employer NICs | Total |

|---|---|---|---|---|---|

| Client | – | 12,460 | 4,853 | 5,943 | 23,256 |

Note: This is calculated using 2022 to 2023 tax rates, thresholds and allowances

However, HMRC will have already collected £7,160 of Corporation Tax and £404 of employer NICs from the PSC, and £2,439 of Income Tax from the worker. As the client is liable to pay the full amount of the Income Tax and NICs due under PAYE, HMRC will have collected an additional £10,003 tax and NICs on the engagement than was due.

Informal consultation to date

HMRC has undertaken a significant amount of informal consultation with key stakeholders on this issue. HMRC has hosted a series of policy development workshops with members of the Employment Status and Intermediaries Forum and employment tax experts (see Annex A for a list of these stakeholders). These workshops were aimed at exploring whether there was a feasible legislative solution that would address this issue and ensure HMRC was collecting the right amount of tax.

This positive and constructive engagement has led to the identification of a possible option, which HMRC has continued to explore and which forms the basis of this consultation.

3. Notifying customers of potential overpayments

HMRC has been considering the options available to it to ensure the correct tax and NICs is being collected overall when errors are found.

HMRC has been looking at how it can address the immediate issue of over-collection by working within its existing powers and laws, whilst exploring whether changes should be made to the legislation.

Current legislation does not allow HMRC to set off amounts of tax and NICs already paid by a worker and their intermediary against the PAYE liability of the deemed employer. Instead, where a worker and their intermediary have paid tax and NICs on income that should have been subject to the off-payroll working rules, they may be entitled to claim a repayment for amounts they have overpaid.

When a compliance check has concluded, HMRC seeks to notify affected workers and their intermediaries if they are entitled to claim a repayment of taxes overpaid in relation to the specific off-payroll working engagement, but only where HMRC has sufficient information to contact them.

To facilitate this process, compliance officers request details from the client of all workers and their intermediaries that are included in the compliance check. Where available, the details collected are used to trace workers and their intermediaries on HMRC’s systems.

Where the worker’s intermediary is a company, it will be notified by letter that the income has now been treated as employment income of the worker and that it may be entitled to overpayment relief for the Corporation Tax it has paid on its business profits. The worker will receive a separate notification about a potential entitlement to claim overpayment relief for the Income Tax and NICs they have paid on any salary received from their company and tax on any dividends also received from their company.

HMRC can only notify workers and their intermediaries once the compliance check has concluded, and the process is only effective where HMRC has enough information from the client to trace the workers and their intermediaries on its systems. Without the full details from the client, HMRC cannot notify workers or their intermediaries of their potential entitlement to overpayment relief and remains in the position of over-collecting tax.

Where a repayment is made, this would result in the right amount of tax being collected overall. However, the worker and PSC does not bear any burden for their tax bills.

Illustrative example of the notification process

The following example aims to illustrate how the notification process works in practice:

-

In 2021 to 2022, a large-sized client directly engages with 100 contractors, working through their own PSCs, to work in their company. The client carries out status determinations on each of these workers and determines that 25 of them are inside the rules, whilst the other 75 are outside the rules.

-

In January 2023, HMRC conducts an enquiry into the client and discovers that of the 75 workers determined as outside the rules, 25 of them were incorrectly determined and were actually working like employees. Therefore, the client should have operated PAYE on payments made to these workers.

-

As part of the compliance check, the client provides HMRC with details of all of these workers and their PSCs so that HMRC can identify them on its systems.

-

HMRC calculates the gross amount of PAYE liability that the client, as the deemed employer, now owes. The client agrees to settle this amount, concluding the compliance check. It can typically take 18 to 21 months to conduct a check, so in this example the case would be concluded around October 2024.

-

HMRC uses the information provided by the client to issue letters to each PSC and worker notifying them of their potential entitlement to a refund of taxes incorrectly paid. If the client has been unable to provide the required information, HMRC will not be able to notify them.

-

The worker and PSC reviews their records and decides if they are due a refund. If they are, they write to HMRC to make an overpayment relief claim or amend their tax returns if in time. An overpayment relief claim must be submitted within four years of the end of the tax year in which the engagement took place, so in this example the deadline is 5 April 2026.

-

If the worker and/or PSC are also entitled to a refund of NICs, they will need to write to HMRC to claim this refund.

-

The claims are received by HMRC and the refund is processed, if it is due. Checks may be carried out on claims to ensure they are correct before a refund is processed.

-

This results in the deemed employer bearing all of the cost of the worker’s tax burden, with the worker bearing none of it.

4. Possible alternative option

This chapter seeks views on an alternative option that HMRC is considering to address the issue of over-collecting tax in cases of non-compliance.

Objectives

In considering how to address this issue, HMRC has identified a number of objectives that a solution should aim to achieve in order to deliver the desired outcome. These objectives are:

-

A solution must continue to incentivise compliance with the off-payroll working rules and encourage clients to take reasonable care and make correct status determinations from the outset.

-

A solution must not result in the client gaining an economic advantage from getting the status determination wrong.

-

The amount to be set against the deemed employer’s PAYE liability must be calculable, either exactly or approximately, using information that is currently available to HMRC or that can be provided by the deemed employer.

-

A solution should share the tax burden more equitably between the deemed employer and worker.

-

HMRC should not collect more tax and NICs than is necessary to achieve the key principles of the off-payroll working rules.

-

A solution should not give rise to obligations and rights that are too difficult to exercise or implement in practice, both for HMRC and taxpayers.

-

A solution should minimise the administrative burden of correcting errors for all parties.

-

A solution should encourage co-operation between HMRC and taxpayers.

HMRC recognises that a solution to this issue may not achieve all of the above objectives and some compromise is likely to be required. With this in mind, HMRC has been looking at a solution that would more effectively address the issue of overcollection by setting off taxes already paid against a subsequent PAYE liability.

Setting off of taxes already paid

Currently, where a worker is engaged through their own PSC, legislation does not allow HMRC to set off taxes already paid by the worker or their PSC against a deemed employer’s subsequent PAYE liability (a ‘set-off’).

To address this, HMRC is considering whether to allow for such a mechanism for off-payroll working purposes. This would potentially work in a similar manner to existing provisions in the PAYE Regulations 2003 (SI 2003/2682), that can allow the setting off of taxes already paid in certain circumstances where HMRC discovers that a directly engaged worker has been incorrectly classed as a self-employed sole trader instead of employed for tax purposes.

Under Regulations 72E-G of the PAYE Regulations, HMRC may make a direction that the employer is not liable to pay an amount of Income Tax due under PAYE where it appears to HMRC that Income Tax on the payment is likely to have been included on the worker’s Self Assessment tax return, or paid on account or deducted under the Construction Industry Scheme (CIS).

These regulations cannot be readily applied to off-payroll working engagements due to challenges associated with having the worker’s PSC between the deemed employer and the worker. This means it is not possible for HMRC to readily determine whether amounts represent Income Tax paid in respect of the payments received from the off-payroll working engagement.

In addition, the PAYE regulations only apply to Income Tax and do not extend to Corporation Tax and Class 1 NICs that may have been paid by a worker’s PSC.

However, in the less common circumstances where a worker is providing their services through a partnership or another individual, and all of the income is reported through the worker’s Self Assessment tax return, a set-off may be possible under Regulations 72E-G.

What taxes will be in scope

This policy would only allow for a set-off to be given against the deemed employer’s liabilities for Income Tax and employee NICs deducted in respect of the worker. It would not be given against any employer NICs due by the deemed employer, or Apprenticeship Levy if applicable.

The worker and their intermediary would not be required to pay any additional tax or NICs as part of this set-off.

The different taxes and classes of NICs that would be included as part of a set-off are:

-

Corporation Tax paid by a worker’s PSC on the income from the off-payroll working engagement

-

Income Tax and employee NICs paid on a salary to the worker from the worker’s intermediary, where the salary is paid out of income from the off-payroll working engagement

-

class 2 and 4 NICs paid by the worker with respect to income from the off-payroll working engagement, where the worker’s intermediary is a partnership or another individual

-

tax paid on dividends received by a worker from their own PSC, where the dividends are paid out of income from the off-payroll working engagement

We do not intend to include the following as a part of any set-off:

-

employer NICs paid by the worker’s intermediary. This is because employer NICs is a distinct and separate charge levied on the employer. The worker’s intermediary is not the employer for the purposes of the off-payroll working rules. Instead, the intermediary would need to claim a refund from HMRC

-

class 3 NICs payments made by the worker. This is because these are voluntary payments that may be made by the worker in certain circumstances

-

tax and NICs paid on any salary and dividends received by any other employees, directors or shareholders of the worker’s intermediary. This is because these payments are not related to the services provided by the worker to the client

Question 1: Do you agree with the taxes that would be included in and excluded from a set-off? If you do not agree, please explain why.

Calculating the tax and NICs already paid

HMRC is currently unable to accurately determine the amount of tax that has been paid by a worker and their intermediary with respect to a particular off-payroll working engagement without further investigation of the worker’s and their intermediary’s tax affairs. These affairs will be unique to each worker and depend on a number of different factors, including: other revenue streams; the intermediary’s accounting period; number of shareholders; number of other employees; and how funds are extracted from the intermediary.

Undertaking this level of investigation can be administratively burdensome, resource intensive and costly for HMRC, deemed employers and workers. To resolve this, HMRC is considering whether to calculate the amount of tax already paid on a reasonable basis using information that is available to it. This means that HMRC would be able to use assumptions and best judgement to estimate the amount of tax paid by a worker and their intermediary that represents tax paid on off-payroll working income.

Assumptions may include determining the amount of personal allowance available, the apportionment of business expenses, whether there are other sources of income (such as other off-payroll working engagements, investment income or property income), distributions to other shareholders, any other available reliefs, as well as other factors.

Where appropriate, HMRC would use relevant tax return data to inform its assumptions and estimates but may also rely on historic patterns of behaviour and tax receipts.

Any assumptions and best judgement should be explained to the deemed employer.

Question 2: Are there any adverse impacts on the deemed employer, the worker or their intermediary as a result of HMRC estimating the amount of the set-off that would be given? If so, please provide details of these impacts.

Question 3: Would giving a set-off have any impacts on other parts of the tax system for either the deemed employer, worker or their intermediary?

Directions and appeals

Where the deemed employer is eligible for a set-off, the worker and their intermediary would be notified via a direction notice that a set-off will be given. The direction notice would not charge any additional tax on the worker or their intermediary. It will inform them that their deemed employer failed to operate PAYE on income received from the off-payroll working engagement, and that some of this PAYE liability is being set off against tax and NICs that the worker and its intermediary has paid via their tax returns.

The worker and their intermediary will not be able to amend their tax returns to claim repayments for amounts that have been set against the deemed employer’s PAYE liability. This prevents a double relief that would result in a loss of tax to the Exchequer.

In a similar manner to the operation of Regulation 72F, the deemed employer would not have a right to appeal against the direction notice or HMRC’s refusal to make a direction. The deemed employer would still be able to appeal against a determination under Regulation 80 for the PAYE liability due.

The worker and their intermediary would have a right to appeal against the direction notice on specific grounds. For example, they would be able to appeal on the grounds that the information contained in the direction notice is incorrect, such as:

-

the worker or their intermediary did not receive a payment from that deemed employer in the tax year or accounting period specified in the direction notice

-

the amount of the tax and NICs to be set off is incorrect, possibly as a result of a change in tax affairs since the direction notice was issued

The worker or their intermediary would not be able to appeal a direction notice on the basis that they disagree with HMRC’s conclusion regarding the status of the worker.

The worker or their intermediary would have 30 days from the date the direction notice is issued to appeal. If they do not appeal within this time limit, the direction will be treated as agreed and the deemed employer’s PAYE liability will be reduced by the amount of the set-off.

Question 4: Do these grounds for appeal provide sufficient safeguards for deemed employers, workers and their intermediaries where they disagree with the direction to set off amounts already paid against their deemed employer’s PAYE liability?

Information required for a set-off

The ability to apply a set-off will depend on whether HMRC can trace the worker and/or their intermediary’s records on its systems. This is because checks will need to be carried out to make sure the worker and their intermediary have submitted tax returns for the relevant years and that tax has been paid. Furthermore, as set out above, HMRC will need to issue direction notices to each worker and their intermediary where a set-off is given.

To facilitate this, HMRC would need to obtain as much information as possible from the client regarding the worker and their intermediary. This could include, but is not limited to:

- the worker’s name and address

- the worker’s date of birth

- the worker’s National Insurance Number (NINO)

- the intermediary’s name and address

- the intermediary’s VAT Registration Number (VRN) or Company Registration Number (CRN)

Ideally, providing a NINO, VRN and/or CRN would be the easiest way of tracing records. Where this cannot be provided, HMRC would need to try and match information that has been made available against its databases. Clients should consider gathering this information as part of their hiring practices.

If HMRC cannot identify a worker or their intermediary on its system, it will not be able to give a set-off. Similarly, if HMRC establishes that no tax return has been submitted, or no tax paid, then no set-off would be given.

Question 5:

A: What information do you, as the client, routinely gather as part of your hiring practices for off-payroll workers?

B: Please provide your views on how easily a client would be able to obtain the above information and provide this to HMRC if requested.

Impacts on compliant behaviour

As set out in the objectives, any solution should continue to incentivise compliance with the off-payroll working rules and encourage clients to take reasonable care in making their status determinations.

Currently, where there is non-compliance with the rules and the engagement is incorrectly treated as outside of the off-payroll working rules, the deemed employer (either the client or an agency in the labour supply chain) will be liable for the full Income Tax and NICs that should have been due. This means the deemed employer has a financial risk of operating the rules incorrectly.

However, if a set-off were to be available, this would potentially reduce this financial risk to the deemed employer, as the Income Tax and NICs liability that the deemed employer will have to pay may be reduced by the tax and NICs already paid by the worker and their intermediary.

Question 6: Would allowing a set-off create any adverse incentives or changes in behaviour amongst clients, or other parties in the labour supply chain, when determining whether the off-payroll working rules should apply?

Penalties where errors are made

Any set-off that reduces the deemed employer’s Income Tax and NICs liability will not affect the application of the penalties regime for inaccuracies. Where there has been an incorrect status determination, HMRC will consider whether to charge a penalty in line with its existing guidance.

Where a penalty is charged, the amount of the penalty will be calculated on the full Income Tax and NICs liability, not the amount after a set-off. This is because the error has still resulted in the full liability becoming due, even though some of this liability is being set-off against amounts already paid by the worker and their intermediary. This is in line with HMRC’s standard approach to penalties in employer compliance checks.

Illustrative example of a set-off

The following example aims to illustrate how a set-off would work in practice:

-

In 2024/25, a large-sized client engages with 100 contractors, working through their own PSCs, to work in their company. The client carries out status determinations on each of these workers and determines that 25 of them are inside the rules, whilst the other 75 are outside the rules.

-

In October 2025, HMRC conducts an enquiry into the client and discovers that of the 75 workers determined as outside the rules, 25 of them were incorrectly determined and were actually working like employees. Therefore, the client should have operated PAYE on payments made to these workers.

-

As part of the compliance check, the client provides HMRC with details of all of these workers and their PSCs so that HMRC can identify them on its systems.

-

HMRC calculates the gross amount of PAYE liability that the client now owes. Next, HMRC looks at whether a set-off can be provided to account for tax that has already been paid by the worker and PSC on that income. HMRC uses the information provided by the client to check that returns have been submitted and tax paid.

-

Once satisfied of this, HMRC will calculate the amount of Corporation Tax, Income Tax, and NICs that has already been paid by using assumptions and its best judgement.

-

Once the set-off has been calculated, HMRC will issue a notice to each worker and PSC informing them that tax has been underpaid on their engagement, with a set-off applied to the client’s PAYE liability for tax they have already paid. They are not allowed to claim this tax back. The worker and PSC would have the opportunity to appeal this decision, to prevent a set-off being given in situations where they did not actually receive the payment or they believe the client is not due a set-off.

-

Assuming no workers or PSCs appeal, HMRC can calculate the final PAYE liability of the client by reducing the gross PAYE liability by the set-off amount. The client then pays the net PAYE liability and HMRC updates its records to reflect this position.

A typical compliance case can take 18 to 21 months to conclude, although it may be shorter or longer depending on the nature and complexity of the case.

5. Application

Subject to a final decision on whether this option is taken forward, the government’s intention would be to implement a legislative solution from 6 April 2024.

The intention is for the policy to apply to Income Tax and NICs liabilities assessed on or after 6 April 2024 which arise as a result of an error in operating the off-payroll working rules in respect of deemed direct payments made from 6 April 2017, when the public sector reform was introduced.

This would replace the process whereby HMRC seeks to notify workers and their intermediaries regarding a potential entitlement to claim a repayment of taxes overpaid.

Settled compliance checks

Where a compliance check has already concluded before 6 April 2024 and the deemed employer has agreed to settle the PAYE liability based on the legislation at the time, this policy would not be applied retrospectively to adjust the deemed employer’s settled PAYE liability. In these cases, HMRC will notify the worker and their intermediary of their potential entitlement to claim a repayment of taxes overpaid, where the information is available.

Question 7: Do you agree with how the government intends to apply this policy?

6. Assessment of impacts

Summary of impacts

| Year | 2022 to 2023 | 2023 to 2024 | 2024 to 2025 | 2025 to 2026 | 2026 to 2027 | 2027 to 2028 |

|---|---|---|---|---|---|---|

| Exchequer impact (£m) | Nil | Nil | Nil | Nil | Nil | Nil |

Exchequer Impact Assessment

This measure is expected to decrease receipts. Costings and forecast adjustments, where required, will be subject to the scrutiny by the Office for Budget Responsibility and included in their forecasts at a future fiscal event.

| Impacts | Comment |

|---|---|

| Economic impact | This measure is not expected to have any significant economic impacts. |

| Impact on individuals, households and families | The proposal will impact individuals who have been incorrectly determined as self-employed for the purposes of the off-payroll working rules. A legislative solution would remove the opportunity for workers to claim a refund for taxes already paid, however they will still pay less tax than would have been due if correctly determined. These individuals will not need to take any action or incur costs, unless they wish to appeal a direction notice. This measure is not expected to impact on family formation, stability or breakdown. This measure is expected overall to have no impact on an individual’s experience of dealing with HMRC as this doesn’t change any processes or tax admin obligations. |

| Equalities impacts | It is not anticipated that there will be impacts on those in groups sharing protected characteristics. |

| Impact on businesses and Civil Society Organisations | The proposal will have an impact on up to 53,000 businesses where it is determined, following a compliance check, that the organisation did not apply the off-payroll working rules correctly. A legislative solution will allow them to claim a set-off for tax paid by a third party against their PAYE liability. One-off costs could include familiarisation with the changes. Continuing costs could include recording more information on the contractors they engage with. There is not expected to be any further continuing costs. This proposal is expected to impact civil society organisations, where they are medium or large in size. This measure is expected overall to improve business’ experience of dealing with HMRC as they will now be able to claim a set-off against their tax liabilities. |

| Impact on HMRC or other public sector delivery organisations | There will be additional resource and administrative impacts on HMRC in applying the legislation to compliance cases, including reviewing customer records, calculating the amount of tax already paid and issuing direction notices to workers and their intermediaries. |

| Other impacts | Other impacts have been considered and none have been identified. |

Question 8: We expect that businesses would need to spend time familiarising themselves with the changes. Can you provide an estimate of the costs your business would expect to incur to familiarise itself with the legislation?

Question 9: Would asking for further information about the worker and their intermediary result in additional ongoing costs to your business? If so, can you provide an estimate for these costs?

Question 10: Please tell us if you think there are any other specific impacts on other groups or businesses that we have not considered above.

7. Summary of consultation questions

Question 1: Do you agree with the taxes that would be included in and excluded from a set-off? If you do not agree, please explain why.

Question 2: Are there any adverse impacts on the deemed employer, the worker or their intermediary as a result of HMRC estimating the amount of the set off that would be given? If so, please provide details of these impacts.

Question 3: Would giving a set-off have any impacts on other parts of the tax system for either the deemed employer, worker or their intermediary?

Question 4: Do these grounds for appeal provide sufficient safeguards for deemed employers, workers and their intermediaries where they disagree with the direction to set off amounts already paid against their deemed employer’s PAYE liability?

Question 5:

A: What information do you, as the client, routinely gather as part of your hiring practices for off-payroll workers?

B: Please provide your views on how easily a client would be able to obtain the above information and provide this to HMRC if requested.

Question 6: Would allowing a set-off create any adverse incentives or changes in behaviour amongst clients, or other parties in the labour supply chain, when determining whether the off-payroll working rules should apply?

Question 7: Do you agree with how the government intends to apply this policy?

Question 8: We expect that businesses would need to spend time familiarising themselves with the changes. Can you provide an estimate of the costs your business would expect to incur to familiarise itself with the legislation?

Question 9: Would asking for further information about the worker and their intermediary result in additional ongoing costs to your business? If so, can you provide an estimate for these costs?

Question 10: Please tell us if you think there are any other specific impacts on other groups or businesses that we have not considered above.

8. The consultation process

This consultation is being conducted in line with the Tax Consultation Framework. There are 5 stages to tax policy development:

Stage 1: Setting out objectives and identifying options.

Stage 2: Determining the best option and developing a framework for implementation including detailed policy design.

Stage 3: Drafting legislation to effect the proposed change.

Stage 4: Implementing and monitoring the change.

Stage 5: Reviewing and evaluating the change.

This consultation is taking place during stage 2 of the process. The purpose of the consultation is to seek views on the detailed policy design and a framework for implementation of a specific proposal, rather than to seek views on alternative proposals.

How to respond

A summary of the questions in this consultation is included at chapter 6.

Responses should be sent by 22 June 2023, by email to [email protected] or by post to:

Off-Payroll Working Policy

3E/4

100 Parliament Street

Westminster

SW1A 2BQ

Please do not send consultation responses to the Consultation Coordinator.

Paper copies of this document or copies in Welsh and alternative formats (large print, audio and Braille) may be obtained free of charge from the above address.

All responses will be acknowledged, but it will not be possible to give substantive replies to individual representations.

When responding please say if you are a business, individual or representative body. In the case of representative bodies please provide information on the number and nature of people you represent.

Confidentiality

HMRC is committed to protecting the privacy and security of your personal information. This privacy notice describes how we collect and use personal information about you in accordance with data protection law, including the UK GDPR and the Data Protection Act (DPA) 2018.

Information provided in response to this consultation, including personal information, may be published or disclosed in accordance with the access to information regimes. These are primarily the Freedom of Information Act 2000 (FOIA), the DPA 2018, UK GDPR and the Environmental Information Regulations 2004.

If you want the information that you provide to be treated as confidential, please be aware that, under the Freedom of Information Act 2000, there is a statutory Code of Practice with which public authorities must comply and which deals with, amongst other things, obligations of confidence. In view of this it would be helpful if you could explain to us why you regard the information you have provided as confidential. If we receive a request for disclosure of the information we will take full account of your explanation, but we cannot give an assurance that confidentiality can be maintained in all circumstances. An automatic confidentiality disclaimer generated by your IT system will not, of itself, be regarded as binding on HM Revenue and Customs.

Consultation Privacy Notice

This notice sets out how we will use your personal data, and your rights. It is made under Articles 13 and/or 14 of the UK GDPR.

Your data

We will process the following personal data:

Name

Email address

Postal address

Phone number

Job title

Purpose

The purposes for which we are processing your personal data is: ‘Off-Payroll Working (IR35): calculation of PAYE liability in cases of non-compliance’.

Legal basis of processing

The legal basis for processing your personal data is that the processing is necessary for the exercise of a function of a government department.

Recipients

Your personal data will be shared by us with HM Treasury.

Retention

Your personal data will be kept by us for 6 years and will then be deleted.

Your rights

You have the right to request information about how your personal data are processed, and to request a copy of that personal data.

You have the right to request that any inaccuracies in your personal data are rectified without delay.

You have the right to request that any incomplete personal data are completed, including by means of a supplementary statement.

You have the right to request that your personal data are erased if there is no longer a justification for them to be processed.

You have the right in certain circumstances (for example, where accuracy is contested) to request that the processing of your personal data is restricted.

Complaints

If you consider that your personal data has been misused or mishandled, you may make a complaint to the Information Commissioner, who is an independent regulator. The Information Commissioner can be contacted at:

Information Commissioner’s Office

Wycliffe House

Water Lane

Wilmslow

Cheshire

SK9 5AF

0303 123 1113 [email protected]

Any complaint to the Information Commissioner is without prejudice to your right to seek redress through the courts.

Contact details

The data controller for your personal data is HMRC. The contact details for the data controller are:

HMRC

100 Parliament Street

Westminster

London

SW1A 2BQ

The contact details for HMRC’s Data Protection Officer are:

The Data Protection Officer

HMRC

14 Westfield Avenue

Stratford

London

E20 1HZ

Consultation principles

This call for evidence is being run in accordance with the government’s Consultation Principles.

The Consultation Principles are available on the Cabinet Office website.

If you have any comments or complaints about the consultation process, please contact the Consultation Coordinator.

Please do not send responses to the consultation to this link.

Annex A: List of stakeholders consulted

- Association of Chartered Certified Accountants (ACCA)

- Association of Independent Professionals and the Self-Employed (IPSE)

- Association of Professional Staffing Companies (APSCO)

- Chartered Institute of Payroll Professionals (CIPP)

- Chartered Institute of Taxation (CIOT)

- Confederation of British Industry (CBI)

- Deloitte

- Ernst & Young

- Freelancer & Contractor Services Association (FCSA)

- Institute of Chartered Accountants in England and Wales (ICAEW)

- Institute of Chartered Accountants of Scotland (ICAS)

- KPMG

- Recruitment and Employment Confederation (REC)

- Tax Centre for Excellence (TCOE)

Annex B: Relevant (current) government legislation

Income Tax (Earnings and Pensions) Act 2003

Chapter 10, Part 2 of Income Tax (Earnings and Pensions) Act 2003

Regulation 72E-G, The Income Tax (Pay As You Earn) Regulations 2003

Regulation 72E(1)

72E(1) Regulation 72F applies where–

(a) one or more employees have received a relevant payment;

(b) it appears to HMRC that an amount intended to represent tax on the payment–

(i) is likely to have been self-assessed by one or more of the employees, or

(ii) has not been self-assessed, but has been paid under section 59A TMA (payments on account of income tax), section 559A of ICTA (treatment of sums deducted under s. 559 (sub-contractors)) or section 62 of the Finance Act 2004 (treatment of sums deducted (sub-contractors));

(c) any of conditions A, B and C is met;

(d) a trigger event has occurred; and

(e) a trigger event did not occur before 6th April 2008.

72E(2) Condition A is that it appears to HMRC that the amount which the employer was liable to deduct–

(a) from the relevant payment; or

(b) in the case of a notional payment, from other relevant payments, exceeds the amount actually deducted.

72E(3) Condition B is that it appears to HMRC that the amount for which the employer was required to account under regulation 62(5) (notional payments) in respect of the relevant payment exceeds the amount actually accounted for.

72E(4) Condition C is that–

(a) tax on the relevant payment was included in a determination under regulation 80 (determination of unpaid tax and appeal against determination); and

(b) the full amount of the determination is not paid within 30 days from the date on which the determination became final and conclusive.

72E(5) The following are trigger events–

(a) HMRC serve notice of a determination under regulation 80 that includes tax on the relevant payment;

(b) HMRC receive a return under section 8 of TMA (personal return) which includes a self-assessment which includes tax on the relevant payment as tax treated as deducted;

(c) HMRC receive–

(i) an amended return under section 9ZA of TMA (amendment of personal or trustee return by taxpayer), or

(ii) a claim under section 33 of TMA (error or mistake), which includes tax on the relevant payment as tax treated as deducted;

(d) HMRC receive a letter of offer.

72E(6) In paragraph (5)–

“letter of offer” means an offer in writing by the employer to agree an amount in settlement of the employer’s liability to pay an amount that includes tax on the relevant payment;

“tax treated as deducted” has the meaning given by regulation 185(6).

72E(7) For the purposes of this regulation tax is self-assessed if–

(a) it is included in a return under section 8 of TMA which includes a self-assessment; and

(b) ignoring any relevant credit, the tax is or would be assessed as payable by way of income tax.

72E(8) In paragraph (7), “relevant credit” means–

(a) a payment made under section 59A of TMA (payments on account of income tax) or 59B (payment of income tax and capital gains tax); or

(b) tax deducted at source or tax treated as deducted (within the meaning given by regulation 185(6)).

Regulation 72F

72F(1) Where this regulation applies, HMRC may direct that the employer is not liable to pay an amount of tax to them.

72F(2) The direction may be in respect of one or more amounts that appear to HMRC to fall within regulation 72E(1)(b)(i) and (ii).

72F(3) A direction must be made by notice to both the employer and the employee, stating–

(a) the date the notice was issued;

(b) the–

(i) amount (or amounts) within regulation 72E(1)(b) to which it relates, or

(ii) employment in respect of which the relevant payment within regulation 72E(1)(a) was received and in respect of which the amount within regulation 72E(1)(b)(i) is likely to have been self-assessed, and

(c) which of conditions A, B and C in regulation 72E have been met.

72F(4) A direction may be combined with one or more other directions relating to the same employer and may be made by issuing one notice to the employer, but each employee must be issued with a separate notice.

72F(5) A notice need not be issued to the employee if neither HMRC nor the employer are aware of the employee’s address or last known address.

72F(6) The amount specified in a notice to the employee must not be added under regulation 185(5) or 188(3)(a) (adjustments to total net tax deducted for self-assessments and other assessments) in relation to the employee.

Regulation 72G

72G(1) An employee may appeal against a direction notice under regulation 72F–

(a) by notice to HMRC, (b) within 30 days of the issue of the direction notice, (c) specifying the grounds of the appeal.

72G(2) For the purposes of paragraph (1) the grounds of appeal are that–

(a) the employee did not receive a relevant payment;

(b) the amount specified in the notice is incorrect, because all or part of it did not fall within regulation 72E(1)(b)(i) or (ii);

(c) no trigger event within regulation 72E(5) occurred; or

(d) a trigger event within regulation 72E(5) occurred before 6th April 2008.

72G(3) On an appeal under paragraph (1) that is notified to the tribunal, the tribunal may–

(a) if it appears that the direction should not have been made, set aside the direction; or

(b) if it appears that the amount specified in the notice is incorrect, increase or reduce the amount accordingly.