Cyber security longitudinal survey: wave 1

Published 27 January 2022

© Crown copyright 2022

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: [email protected].

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/cyber-security-longitudinal-survey-wave-one/cyber-security-longitudinal-survey-wave-1

Executive summary

The Cyber Security Longitudinal Survey (CSLS) aims to better understand cyber security policies and processes within medium and large businesses and high-income charities, and to explore the links over time between these policies and processes and the likelihood and impact of a cyber incident. This is the first research year of a three-year study, and therefore the main objective of this report is to establish a baseline of findings as a precursor to further reports in subsequent research waves. This report also summarises additional insight from 30 follow-up qualitative interviews with survey respondents, that covered topics such as cyber security resilience, ransomware, record keeping, internal and external reporting, responsibility for cyber security and monitoring of supply chains. These are intertwined with reporting on quantitative findings.

Overall, this baseline study found that the cyber resilience profile of organisations varies between businesses and charities as well as by business size and sector. Businesses are more likely than charities to have formal, written cyber security policies and processes in place. Large businesses (250+ staff), and particularly very large businesses (500+ staff), demonstrate greater cyber maturity compared to medium businesses and charities. Additionally, businesses in the finance and insurance and information and communication sectors tend to be in the lead in terms of cyber maturity. However, overall, organisations’ approach to cyber is likely to be more reactive than proactive, with many struggling to get senior level buy-in to improve their cyber defences. Below is a more detailed summary of key findings from each chapter of this report.

The survey results are subject to margins of error, which vary with the size of the sample and the percentage figure concerned. For all percentage results, subgroup differences by size, sector and survey answers have been highlighted only where statistically significant [footnote 1] (at the 95% level of confidence).

Board involvement

This chapter investigates the level of awareness and engagement with cyber security among board members. In most organisations, members of the board are unlikely to be involved in decisions or discussions around cyber security. Half of businesses (50%) and four in ten charities (40%) say they have one or more board members whose roles include oversight of cyber security risks. Additionally, only around one-third of businesses (37%) and charities (32%) have board-level discussions or updates on cyber security at least quarterly. On a related note, a relatively low proportion of businesses (35%) and charities (28%) say their board members have received any cyber security training.

However, among organisations where some form of board-level discussions about cyber security do happen, more than half of businesses (55%) and charities (60%) agree that their board integrates cyber risk considerations into wider business areas. This, together with findings from the qualitative interviews, suggests that the main problem is not in management taking ineffective action, but a lack of engagement from senior management in the first place.

Sources of information

This chapter identifies key information sources used to inform organisations’ approach to cyber security in the last year.

Around one-third (32%) of charities and one-quarter (23%) of businesses say they have used information or guidance from the National Cyber Security Centre (NCSC) to inform their approach to cyber security in the last year. Very large businesses with 500+ employees (37%), and businesses in the finance and insurance (51%) and information or communication (41%) sectors are the most likely to use NCSC guidance. In the qualitative research, participants mentioned that they had found the NCSC a useful source of information.

Regarding other sources of information or influences on cyber security policies and processes, feedback from external IT or cyber security consultants has influenced 47% of businesses and 55% of charities in the last twelve months.

Cyber security policies

This chapter sets the baseline of cyber security policies within our longitudinal sample. Monitoring any changes to these policies over time will help us better understand how organisations are evolving their cyber defences. It will also help explore the impact this may have on organisations’ resilience to incidents.

When asked about various documentation in place to help manage cyber security risks, businesses and charities are both most likely to say that they have a Business Continuity Plan covering cyber security (69% and 73% respectively), while they are least likely to have documentation outlining how much cyber risk their organisation is willing to accept (26% and 31% respectively). Fewer than one in five organisations (17% of both businesses and charities) report having all five of the types of documentation[footnote 2] asked about in place – although the proportion of large businesses who have all five is higher (21%). During the qualitative interviews, respondents frequently suggested that they follow informal, ‘common sense’ processes when it comes to dealing with incidents rather than using formal, written policies or processes.

Having some form of cyber insurance cover is relatively common among both businesses and charities. Overall, charities are more likely than businesses to say they have some form of cyber insurance (66% vs. 53% respectively), and there is little difference by size of business (57% of large and 52% of medium businesses). Having cyber security cover as part of a broader insurance policy is more common than having a specific cyber insurance policy across both businesses and charities.

Around half of charities and businesses say they have carried out cyber security training or awareness raising sessions in the last twelve months for any staff (or volunteers) who are not directly involved in cyber security (55% and 48% respectively). This suggests that carrying out cyber security training is unlikely to be a universal practice, although staff training is more common among large businesses (250+ staff) (60%). During the qualitative interviews it was typical for organisations to say they had never assessed the cyber skills of their workforce and had limited understanding of what this would cover or its value for the organisation.

Cyber security processes

This chapter provides insight on the uptake of cyber security certifications by organisations. It also sets the baseline for the cyber security processes that organisations have in place, the technical controls required to attain Cyber Essentials certification, and actions taken over the last twelve months to improve or expand various aspects of organisations’ cyber security.

Most organisations do not have cyber security certifications. For example, just one in five (19% among both businesses and charities) say they are certified under the Cyber Essentials standard, which is the most frequently obtained certification.

Large businesses (250+ staff) are more likely to adhere to some form of cyber security certification (e.g., 19% of large businesses comply with ISO 27001 compared to 14% of medium businesses), and there are also clear sectoral differences in terms of the types of certifications businesses pursue. For example, businesses in the information or communications sector are more likely to have all three of the certifications asked about. Almost half (47%) of these have ISO 27001, 42% are Cyber Essentials certified, and 27% have Cyber Essentials Plus. Reasons for obtaining certifications varied during the qualitative interviews, with drivers including contractual requirements, change in senior personnel and having a new IT supplier.

Organisations are taking action to improve their cyber defences and risk management, but this is still limited depending on the nature of the organisation and resources available. Businesses and charities are equally likely to have technical controls in all five of the areas required to attain Cyber Essentials certification[footnote 3] (57% for both), though this increases to 64% of large businesses. Despite having these processes in place, few organisations report including anything about cyber security in their most recent annual report, with 14% of businesses and 18% of charities saying this, and around three times as many businesses and charities (45% and 57% respectively) saying they did not.

Around four in five businesses (79%) and charities (84%) say they have taken at least one form of action to expand some aspect of their cyber security over the last twelve months. Regarding specific measures, more than half of organisations say they have expanded or improved their network security (62% of businesses and 66% of charities), processes for user authentication and access control (59% of businesses and 62% of charities), and their malware defences (55% each). Large businesses are more likely to report having made improvements in these areas over the last year than medium businesses. Hence, while organisations are taking action to be better prepared for and protected against incidents, most have gaps in their cyber hygiene and risk management processes.

Regarding cyber security processes in the supply chain, three in five organisations (60% of businesses and 64% of charities) say they did not carry out work in the last twelve months to formally assess or manage the potential cyber security risks presented by their suppliers.

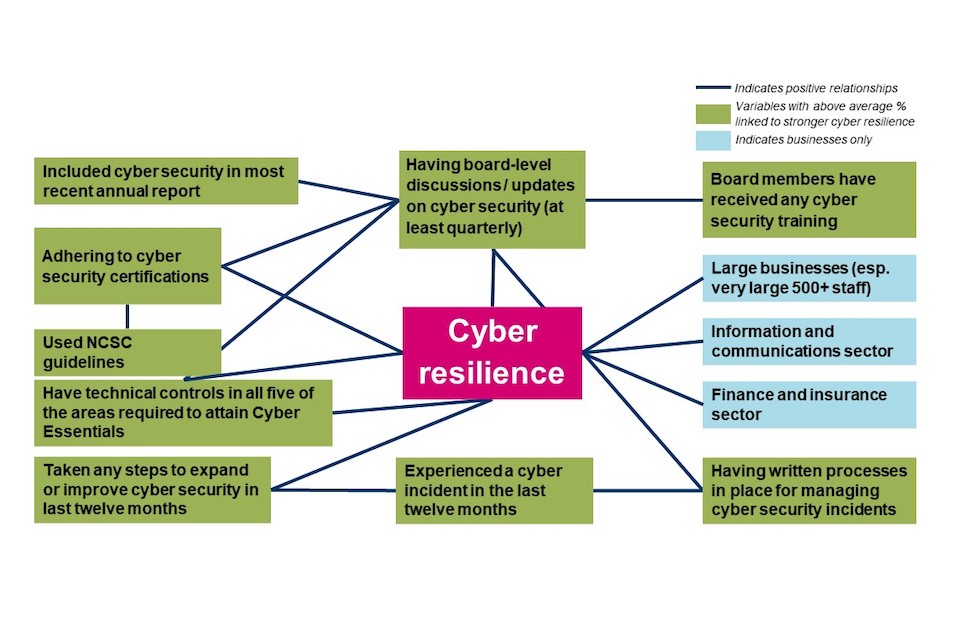

There is a positive relationship between greater board involvement (i.e., more frequent board-level discussions or updates about cyber security) and having in place all five of the technical controls required to attain Cyber Essentials certification. There is also a positive relationship between board involvement and having processes in place to assess or manage cyber security risks presented by suppliers. For example, 68% of businesses with at least monthly board-level discussions and updates about cyber security have technical controls in place in all five of the areas required to attain Cyber Essentials, compared to 36% of businesses that never have board-level discussions and updates. This is similar for charities. In line with other findings, this suggests that buy-in from senior management is likely to have a positive impact on the kind of cyber defences in place. Additionally, businesses that experienced a cyber incident in the last twelve months are also more likely to have technical controls in place in all five of the areas required to attain Cyber Essentials (62% vs. 50% of businesses not reporting an incident).

Cyber incident management

This chapter captures the proportion of organisations that have written processes for cyber security incident management and what these may cover.

Businesses and charities are equally likely to have written processes for how to manage a cyber security incident (51% for each), although the likelihood of having these processes in place is higher among large businesses (250+ staff) (60%).

Additionally, having experience of a cyber security incident over the last twelve months is linked with a higher likelihood of having written processes in place. Just over half (54% of businesses and 55% of charities) of those experiencing an incident in the last twelve months say they have written processes for how to manage a cyber security incident, compared to 44% of both businesses and charities that have not experienced an incident in the last year. This link was implied during the qualitative interviews as well, with respondents often suggesting that experiencing an incident is among the main triggers for introducing formalised cyber security measures. Among organisations with written processes in place, these are most likely to cover guidance for reporting incidents externally, for instance to regulators or insurers (77% of businesses and 86% of charities).

During the qualitative interviews, participants tended to refer to having informal processes in place, with an incident response plan among those, and the level of detail within these procedures and documents was varied.

Prevalence and impact of cyber incidents

This chapter looks at the different kinds of cyber incidents experienced by organisations and their impact and outcome.

Around half (50% of businesses and 47% of charities) say they experienced at least one cyber security incident – excluding phishing – in the last twelve months. This rises to 72% among businesses and 74% of charities when phishing is included.

Among organisations that reported cyber security incidents over the last twelve months, around four in five businesses and charities say that more than one incident happened during this time period (83% and 81% respectively), and this proportion is similar even when phishing incidents are excluded (79% of businesses and 83% of charities).

Around three in ten businesses (29%) and two in ten charities (19%) that experienced non-phishing incidents in the last year say they experienced an incident at least once a week.

Although most incidents have a short-term impact on operations, of those surveyed, around one in ten organisations (8% of businesses and 10% of charities) that experienced an incident in the last twelve months report that it took a day or longer to restore business operations back to normal. Conversely, nine in ten organisations (90% of businesses and 89% of charities) that experienced any incidents report that it took them less than a day to restore business operations back to normal.

Summary of findings

The summary table of key measures in Annex A shows some of the key baseline metrics, split by business size (50-249, 250-499 and 500+ employees). Further details on statistical reliability and margins of error can be found in Annex C.

Chapter 1 – Introduction

1.1 Background to the research

Publication date: 27 January 2022

Geographic coverage: United Kingdom

The Department for Digital, Culture, Media and Sport (DCMS) commissioned the Cyber Security Longitudinal Survey of medium and large UK businesses (50+ employees) and high-income charities (annual income of more than £1m) as part of the National Cyber Security Programme. The findings will evaluate long-term links between the cyber security policies and processes adopted by these organisations, and the likelihood and impact of a cyber incident. It also supports the Government to shape future policy in this area, in line with the National Cyber Strategy 2022, and will inform future government Cyber interventions and support future strategies with quality evidence.

There will be three annual waves of this study. Due to the longitudinal nature of the study, where the aim is to track trends over time, we will largely speak with the same organisations in each wave. This report is based on wave one (2021) data that will provide a baseline for future waves. The design of this research was influenced by a study DCMS previously commissioned to investigate the feasibility of creating a new longitudinal study of large organisations.

The core objectives of this study are to:

-

Explore how and why UK organisations are changing their cyber security profile and how they implement, measure and improve their cyber defences

-

Provide a more in-depth picture of larger organisations, covering topics that are lightly covered in the Cyber Security Breaches Survey (CSBS), such as corporate governance, supply chain risk management, internal and external reporting, cyber strategy, cyber insurance and ransomware

-

In following waves, explore the effects of actions adopted by organisations to improve their Cyber Security on the likelihood and impact of a cyber incident

The results from this study complement findings from the Cyber Security Breaches Survey (CSBS), an annual study of UK businesses, charities and education institutions as part of the National Cyber Security Programme, as both studies explore UK Cyber Resilience and therefore help to inform and shape government activity in this area.

1.2 Difference from the Cyber Security Breaches Survey

This study differs from the Cyber Security Breaches Survey (CSBS) in multiple important respects. Firstly, it uses a longitudinal approach, where the aim is to track changes in cyber resilience over time, whereas the CSBS uses a cross-sectional sample that provides a snapshot of cyber resilience. This three-year longitudinal study will collect data from the same unit (businesses or charities) on more than one occasion, to analyse the link between large and medium organisations’ cyber security behaviours and the extent to which they influence the impact and likelihood of experiencing an incident over time. In comparison, results from CSBS track changes over time, and provides a static view of cyber resilience at a given time.

Secondly, this survey focuses only on medium and large businesses and high-income charities whereas the CSBS includes all businesses (micro, small, medium, and large), all charities and educational institutions. Additionally, different questions are used, so while there are some similarities in the questions and topics covered by the two surveys, results are not comparable. Finally, as previously discussed, the two studies have different objectives.

The CSBS is an official government statistic, and representative of all UK businesses, charities and educational institutions. Therefore, for overall statistics on cyber security, results from CSBS should be used. Further detail on overlapping questions can be found in the Cyber Security Longitudinal Survey Technical Report.

Please visit the gov.uk website to see publications of the Cyber Security Breaches Survey.

1.3 Methodology

There are two strands to the Cyber Security Longitudinal Survey:

-

Ipsos MORI undertook a random probability multimode (telephone and online) survey of 1,205 businesses (1,051 telephone and 154 online) and 536 UK registered charities (454 telephone and 82 online) from 9 March to 7 July 2021. The data for businesses and charities have been weighted to be statistically representative of these two populations. [footnote 4]

-

Subsequently, 30 in-depth interviews were conducted in July and August 2021, to gain further qualitative insights from some of the organisations that answered the survey. [footnote 5]

This longitudinal study aims to track changes over time, so will follow the same organisations in all three annual waves. In wave one, 1,405 organisations (955 businesses; 450 charities) agreed to be recontacted in wave two, and the aim is to retain at least half of these in the panel in wave two (Spring 2022). In subsequent years there will be an additional cross-sectional sample to supplement the longitudinal sample.

The target population of this research is medium and large businesses and high-income charities. This is due to these organisations being more likely than their smaller counterparts to have specialist staff dealing with cyber security, and to have formal policies and processes covering cyber security risks. Additionally, according to the feasibility study conducted prior to this research, similar proportions of medium and large businesses experienced cyber security incidents within the last twelve months, and both report a higher rate than smaller organisations. Therefore, these organisations provide the most insight into how UK organisations are currently managing their Cyber Security.

To draw the sample, random probability sampling was used to avoid selection bias. The business sample was proportionally stratified by region, and disproportionately stratified by size and sector. More technical details and a copy of the questionnaire are available in the separately published Technical Annex.

1.4 Profile of survey respondents

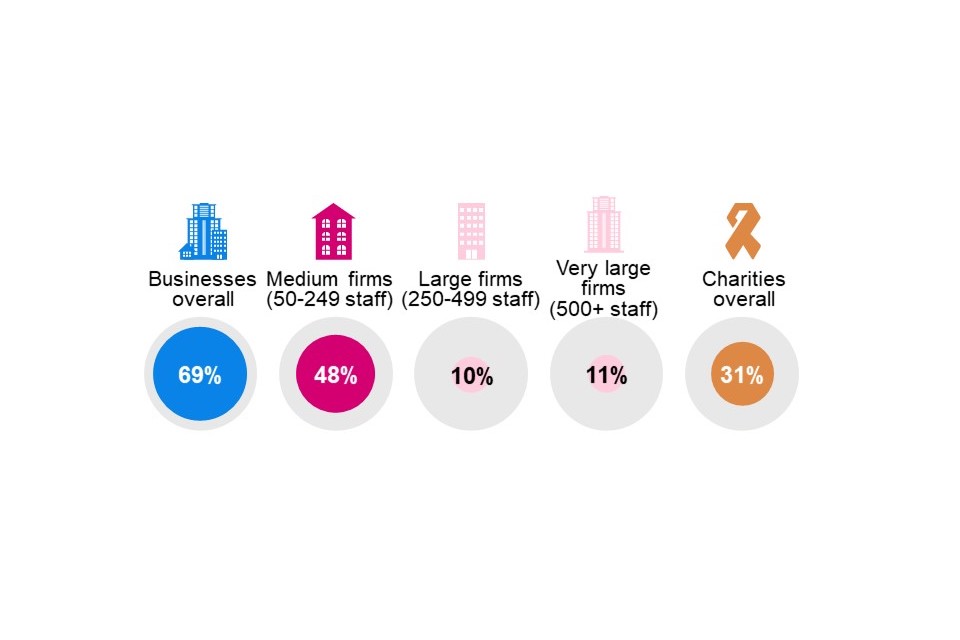

Figure 1.1 Businesses and charities overall and by business size (showing weighted %)

Base: All businesses (n=1,205); Medium firms (n=835); Large firms (n=173); Very large firms (n=197); All charities (n=536).

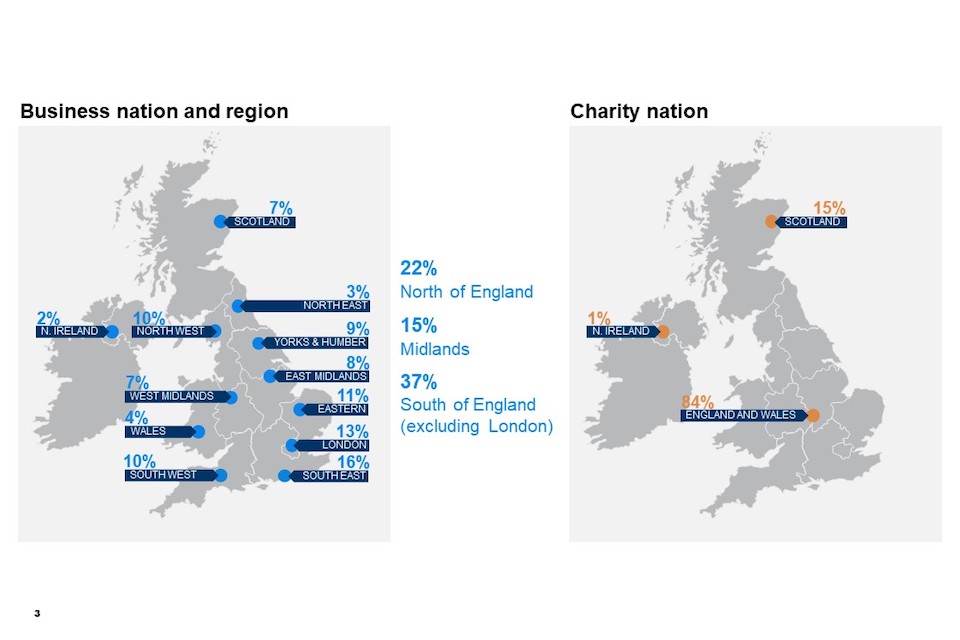

Figure 1.2: Businesses and charities by nation and region (showing weighted %)

Base: All businesses (n=1,205); All charities (n=536). Businesses in East Midlands (n=98); Eastern England (n=126); London (n=162); North East (n=35); North West (n-124); Northern Ireland (n=26); Scotland (n=81); South East (n=196); South West (n=124); Wales (n=46); West Midlands (n=86); Yorkshire and Humber (n=101); Charities in England and Wales (n=451); Northern Ireland (n=7); Scotland (n=78).

Figure 1.3: Businesses by sector (showing weighted %)

Base: All businesses (n=1,205); Administration and real estate (n=155); Construction (n=63); Education (n=36); Entertainment, service and membership organisations (n=10); Finance and insurance (n=50); Food and hospitality (n=116); Health, social care and social work (n=105); Information and communications (n=107); Professional, scientific and technical (n=92); Retail and wholesale(n=174); Transport and storage (n=64); Utilities and production (n=207)

1.5 Profile of qualitative respondents

Thirty follow-up interviews were carried out with a select number of organisations that completed the survey. They were asked to participate based on the following characteristics:

Table 1.1 Profile of qualitative respondents

| Quota | Requirement | Achieved |

|---|---|---|

| Type | Businesses | 18 |

| Charities | 12 | |

| Business – size by staff | Medium (50-249) | 7 |

| Large (250-499) | 5 | |

| Very large (500+) | 6 | |

| Business – sector | Good mix across sectors | 18 |

| Business – region | Good mix across regions | 18 |

| Charity – region | Scotland | 3 |

| England and Wales | 9 |

1.6 Cyber roles and responsibilities

Both the survey and the follow-up qualitative interviews were targeted at the person with the most responsibility for cyber security in the organisation. However, in practice, many organisations don’t have a specific person responsible for cyber security, so interview participants had a wide range of roles and responsibilities which often spread beyond cyber security or even IT. This was particularly the case among organisations that do not have their own IT department.

Large businesses (especially those in the very large category) are more likely to have employees with dedicated IT roles and larger IT teams than medium businesses or charities that often tend to fully outsource IT activities. Although there were some variances among large businesses in this by sector.

Among respondents with a more general, or sometimes non-IT specific role, awareness of cyber security issues tended to be lower. As a result, people at organisations with the most responsibility for cyber security are often stretched and as a result, cyber security tends to be low in their order of priorities. These participants frequently mentioned having full trust in their IT suppliers when it comes to processes and policies mitigating against any incidents, as well as in incident recovery. Not having dedicated cyber security or IT personnel in place was often explained by lack of resources both in terms of finances and skills:

“Being a small business, we outsource a lot of highly specialised things […] I’m the head of IT but, I’m the CSO as well so I have to wear many hats with it being quite a small business.”

Business, Medium, Finance and insurance

Additionally, proportionality was also frequently mentioned, with those from medium businesses or charities suggesting that the cyber security risk faced by the organisation is low compared to a larger organisation or an organisation in the technology sector.

“I’m hoping that the size of our business means that we go below the radar.”

Business, Medium, Construction

1.7 Interpretation of findings

How to interpret the quantitative data

The survey results are subject to margins of error, which vary with the size of the sample and the percentage figure concerned. For all percentage results, subgroup differences by size, sector and survey answers have been highlighted only where statistically significant (at the 95% level of confidence). [footnote 6]

There is a further guide to statistical reliability at the end of this report.

Subgroup definitions and conventions

For businesses, analysis by size splits the population into medium businesses (50-249 employees) and large businesses (250+ employees) . Large businesses were compiled of large (250-499 employees) and very large businesses (500+ employees). All charities have a reported annual income of at least £1 million. [footnote 7]

Due to the relatively small sample sizes for certain business sectors, these have been grouped with other similar sectors for more robust analysis. Business sector groupings referred to across this report, and their respective SIC 2007 sectors, are:

- Administration and real estate (L and N)

- Construction (F)

- Education (P)

- Health, social care and social work (Q)

- Entertainment, service and membership organisations (R and S)

- Finance and insurance (K)

- Food and hospitality (I)

- Information and communications (J)

- Utilities and production (including manufacturing) (B, C, D and E)

- Professional, scientific and technical (M)

- Retail and wholesale (including vehicle sales and repairs) (G)

- Transport and storage (H).

Where figures are marked with an asterisk (*) these refer to base sizes smaller than 50 and should be treated with caution.

1.8 Acknowledgements

Ipsos MORI and DCMS would like to thank all the organisations and individuals that participated in the survey. We would also like to thank the organisations that endorsed the fieldwork and encouraged businesses and charities to participate, including:

- The National Cyber Security Centre (NCSC)

- The Home Office

- The Scottish Government

- The Charity Commission

- The Confederation of British Industry (CBI)

- The Institute of Chartered Accountants in England and Wales (ICAEW)

Chapter 2 – Cyber profile of organisations

This chapter explores the cyber profile of organisations, if they use cloud computing, use of personal devices, and use of Artificial Intelligence (AI) and machine learning.

2.1 Cloud computing

Almost all organisations (97% of businesses, and 95% of charities) use at least one form of secure network to store or access their data and files. Charities (77%) are more likely than businesses (68%) to have a cloud server that stores their data or files. However, businesses (82%) are more likely than charities (72%) to have their own physical server that stores their data or files, and they are also more likely to have a virtual private network (VPN) for staff when they connect remotely (73% of businesses; 66% of charities). [footnote 8]

Figure 2.1: How organisations store or access their data and files

| Does your organisation use or provide any of the following? | Businesses | Charities |

|---|---|---|

| Your own physical server that stores your data or files | 82% | 72% |

| A virtual private network, or VPN, for staff connecting remotely | 73% | 66% |

| A cloud server that stores your data or files | 68% | 77% |

Base: All businesses (n=1,205); All charities (n=536). Don’t know not shown.

2.2 Use of personal devices

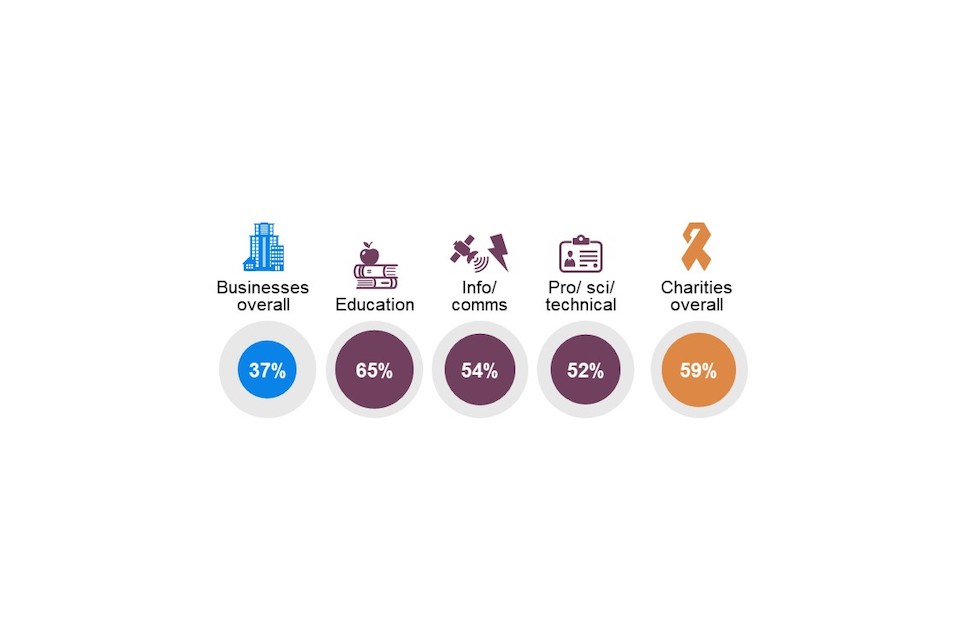

Charities (59%) are more likely than businesses (37%) to permit staff to access their organisation’s network or files through personally owned devices such as a personal smartphone or home computer.

Businesses in the education (65%), information and communications (54%) and professional, scientific and technical (52%) sectors are more likely to permit their staff to use personally owned devices.

Figure 2.2: Use of personal devices to access organisation’s network or files

Are staff permitted to access your organisation’s network or files through personally owned devices? (% Yes)

Base: All businesses (n=1,205); Education sector (n=36*); Information and communications sector (n=107); Professional, scientific or technical sector (n=92); Businesses in London (n=162); All charities (n=536). Don’t know not shown.

Of the organisations that use a VPN, businesses (79%) are more likely than charities (72%) to require their staff to connect via a VPN when connecting to the organisation’s network or files outside of the workplace.

Businesses in the retail and wholesale (90%) and utilities and production (84%) sectors are the most likely to require their staff to connect via a VPN, while those in the health, social care and social work sector (58%) are the least likely to do this.

Businesses and charities that have technical controls in place in all five of the areas required to attain Cyber Essentials are more likely to require staff to connect via a VPN (84% and 76% respectively) than those without technical controls in place in all five of the areas required to attain Cyber Essentials (72% of businesses and 66% of charities).

Figure 2.3: Use of VPN

| If staff connect to your network or files outside your own workplaces, are they forced to connect via a VPN, or can they access your network or files without a VPN? | Forced to connect via a VPN | Can connect without a VPN | Not applicable/ no remote working | Don’t know | Total |

|---|---|---|---|---|---|

| Businesses | 79% | 13% | 3% | 5% | 100% |

| Charities | 72% | 21% | 1% | 5% | 100% |

Base: All businesses (n=1,205); All charities (n=536).

2.3 Use of artificial intelligence (AI) and machine learning

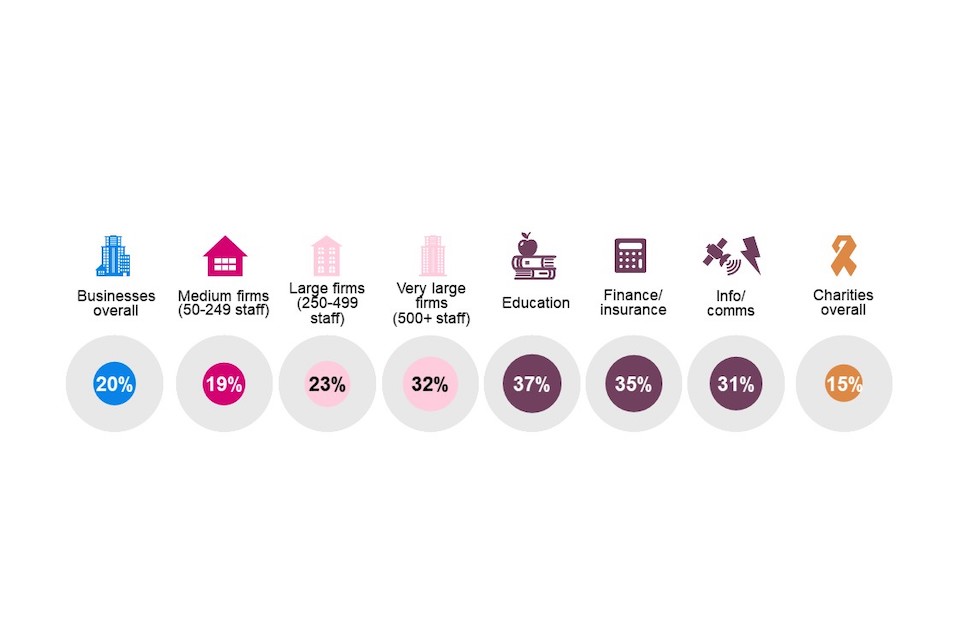

AI is very important to cyber security because pattern recognition algorithms can be applied to network data flows to automate threat detection. Machine learning is a subset of AI that can be used to ‘learn’ any new patterns it identifies from recent incidents. Businesses (20%) are more likely than charities (15%) to use cyber security tools that use AI or machine learning. Almost one in three very large businesses with 500+ employees (32%) deploy AI or machine learning, compared to around one in five medium-sized businesses (19%). Businesses in the education (37%), finance and insurance (35%) and information and communications (31%) sectors are also more likely to deploy AI or machine learning.

Figure 2.4: Use of AI or machine learning

Does your organisation deploy any cyber security tools that use AI or machine learning? (% yes)

Base: All businesses (n=1,205); Medium firms with 50-249 employees (n=835); Large firms with 250-499 employees (n=173); Very large firms with 500+ employees (n=197); Finance and insurance sector (n=50); Education sector (n=36); Information and communications sector (n=107); Businesses in London (n=162); All charities (n=536). Don’t know not shown.

2.4 Use of external IT providers

During the qualitative interviews, businesses and charities were asked whether they use external IT suppliers or cyber security consultants. Some organisations, particularly medium businesses and charities, choose to either completely outsource their IT to an external provider, so they have limited responsibility for it in-house, or they use outsourcing to complement their internal IT teams, for example, when out of hours, for advice or for specific services (e.g. penetration tests).

These relationships are often long-established and involve a high level of trust in these external partners. Additionally, organisations often consider their external IT providers to be an essential part of the organisation.

When asked about how IT suppliers were chosen, most have long-standing relationships with suppliers and limited recall on how the contract started. As a result, many are unlikely to regularly review contracts or shop around for other suppliers.

Outsourcing IT is a decision most often motivated by cost savings, with many respondents suggesting that due to the size of their organisation, having an in-house IT function or capability would be less cost-effective:

“It was a tactical decision to have that rather than having more IT manpower in the department. It was more cost effective to have a partner helping us.”

Business, Large, Professional, scientific and technical

Chapter 3 – Board involvement

This section covers the roles and responsibilities of board members in relation to cyber security in larger organisations. It explores the ways in which board members engage with cyber security, and their frequency.

3.1 Roles and responsibilities

Businesses are more likely than charities to report having one or more board members with an oversight of cyber security risks (50% vs. 40% respectively). In comparison, a higher proportion of charities than businesses (61% vs. 55% respectively) say they have a designated staff member responsible for cyber security, who reports directly to the board. Around three in ten charities (32%) and businesses (30%) report having neither.

Figure 3.1: Cyber security roles and responsibilities within organisations

| Does your organisation have any of the following? | Businesses | Charities |

|---|---|---|

| One or more board members whose roles include oversight of cyber security risks | 50% | 40% |

| A designated staff member responsible for cyber security, who reports directly to the board | 55% | 61% |

| None of these | 30% | 32% |

Base: All businesses (n=1,205); All charities (n=536). Don’t know not shown.

Large businesses (250+ staff) are more likely than medium businesses to report having board members with an oversight of cyber security risks (57% vs. 48% respectively) and a designated staff member who reports directly to the board about these issues (61% vs. 54% respectively). In turn, while three in ten medium businesses (31%) say they have neither, this applies to just 24% of large businesses.

Businesses in the finance and insurance and information and communication sectors are the most likely to have board members with an oversight of cyber security risks (76% and 66% respectively), and a designated staff member who reports directly to the board about these issues (75% and 69% respectively). Businesses in the food and hospitality sector are the least likely to have these, with two in five (41%) reporting having neither.

Across businesses and charities, during the qualitative interviews, respondents often mentioned a lack of understanding from board members around cyber security during the qualitative interviews. This was associated with a variety of interconnected factors, including the age of board members, lack of IT literacy or lack of board-level training opportunities on cyber security. As a result, respondents, who often personally identified as the ‘designated staff member’ reporting directly to the board about cyber security issues, frequently cited communication barriers and/or knowledge gaps when it comes to having conversations about cyber security with board members:

“Our CEO is diligent, interested [in cyber security], but not particularly IT literate. Our Board is interested, but absolutely IT illiterate.”

Charity

In line with the quantitative findings, respondents from certain sectors, such as the food industry and retail, mentioned the issue of board members seeing cyber security as irrelevant for their sector. In comparison, respondents from sectors that tend to be more cyber-oriented, such as the information and communication sector, suggested that their board is likely to be invested in issues related to cyber security, due to historically seeing this as a highly relevant issue for the sector. However, particularly for medium businesses, board-level discussions about cyber security are likely to remain informal, regardless of the level of interest among board members:

“The chairman has a very keen interest, he worked in IT and cyber positions before. He occasionally reaches out and we have more informal discussions. I do have conversations with the chairman about how he wants things to be reported, what he sees as the issues, and [I] do the same with [the] CFO. For a business our size, it works well like that.”

Business, Medium, Information and communications

Businesses that have technical controls in place in all five of the areas required to attain Cyber Essentials, and those with some form of cyber security certification, are more likely than businesses on average to have individuals with these roles and responsibilities within the organisation.

Additionally, businesses that have experienced a cyber incident in the last twelve months are more likely than those that have not to have board members with an oversight of cyber security risks (54% vs. 45% respectively) and a designated staff member who reports directly to the board about these issues (59% vs. 48% respectively).

An increase in interest from board members, and therefore appetite for cyber security certifications, was mentioned by some respondents during the qualitative interviews. These interviews also suggested that personal experience of cyber incidents or increased awareness due to a high-profile case in the news sometimes triggers increased interest from board members and prompts buy-in to cyber certifications. This suggests that board involvement and acquisition of cyber security certification tends to be reactive rather than proactive.

“They want everything in layman’s terms, they don’t want any technicalities at all. The best way would be me saying to them ‘if you don’t do this and something happens, this would be the likely scenario.’ […] They want to see in black and white for cost justification. If you can make a decent case for it, generally it’s going to go through.”

Business, Large, Administration and real estate

“I think they are pretty good. If you look at the university hack which happened, it opened a lot of eyes to the impact it could have. All of the trustees are in industries that involve technology.”

Charity

3.2 Awareness and training

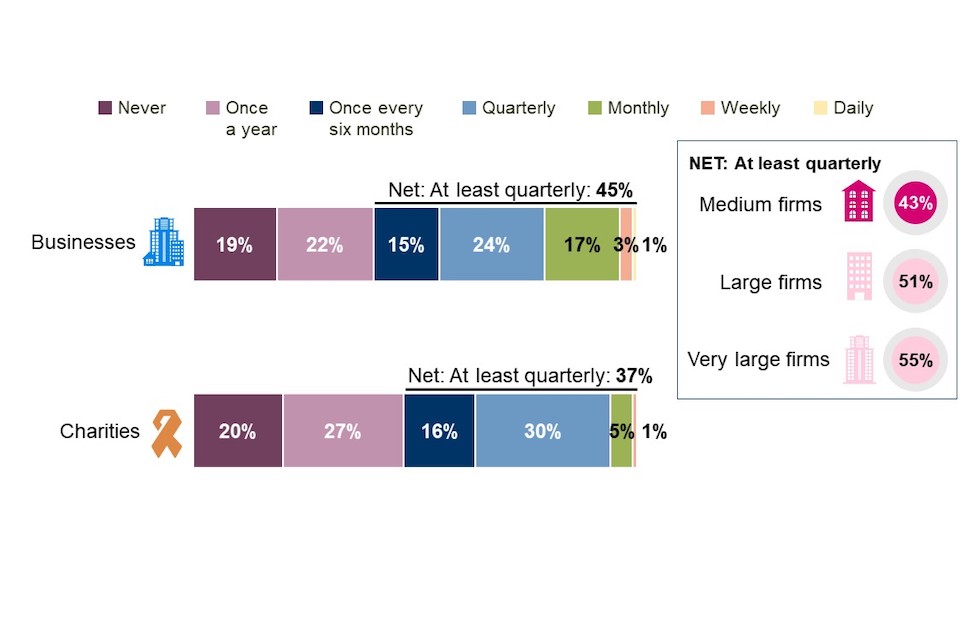

When asked about roughly how often their board discussed or received updates on cyber security over the last twelve months, almost half (45%) of businesses say they did so at least quarterly (excluding don’t know responses). Businesses are more likely to have more frequent board discussions or updates than charities, with 37% of charities reporting that their board had done so at least quarterly.

Figure 3.2: Frequency of board discussions or updates on cyber security

Over the last twelve months, roughly how often, if at all, has your board discussed or received updates on your organisation’s cyber security?

Base: All businesses excluding don’t know (n=974); All charities excluding don’t know (n=473).

Looking across business sizes and sectors, very large businesses with 500+ employees (55%) and businesses in the finance and insurance (81%) and information and communications (74%) sectors are more likely to report having at least quarterly board discussions or updates about cyber security than businesses on average.

While this suggests that board members are likely to have a relatively high level of awareness of cyber security-related issues within organisations, one in five organisations (19% of businesses and 20% of charities) say the board had no such discussions or updates at all over the last twelve months. Non-engagement with cyber security issues, and IT more generally, was also frequently cited during the qualitative interviews, suggesting that even in organisations where discussions do happen, board members tend to have little to no interest or understanding of these issues.

A re-emerging theme during the qualitative interviews with respondents from medium-sized businesses was explaining the lack of interest among board members as often stemming from the culture of the organisation not evolving with growth and expansion. As a result, unless any incidents happen with a notable financial impact, cyber security is likely to be regarded as an issue outside of the board’s remit and of lower priority than other risks:

“They [MD and General Manager] are happy to leave the paranoia to me and the IT Department. They are too busy running the rest of the business.”

Business, Medium, Utilities and production

“There just haven’t been any incidents apart from the one that happened a few weeks ago. Everyone was aware of it because everyone had to change their password. Everyone was briefed and that was an end to it.”

Business, Medium, Transport and storage

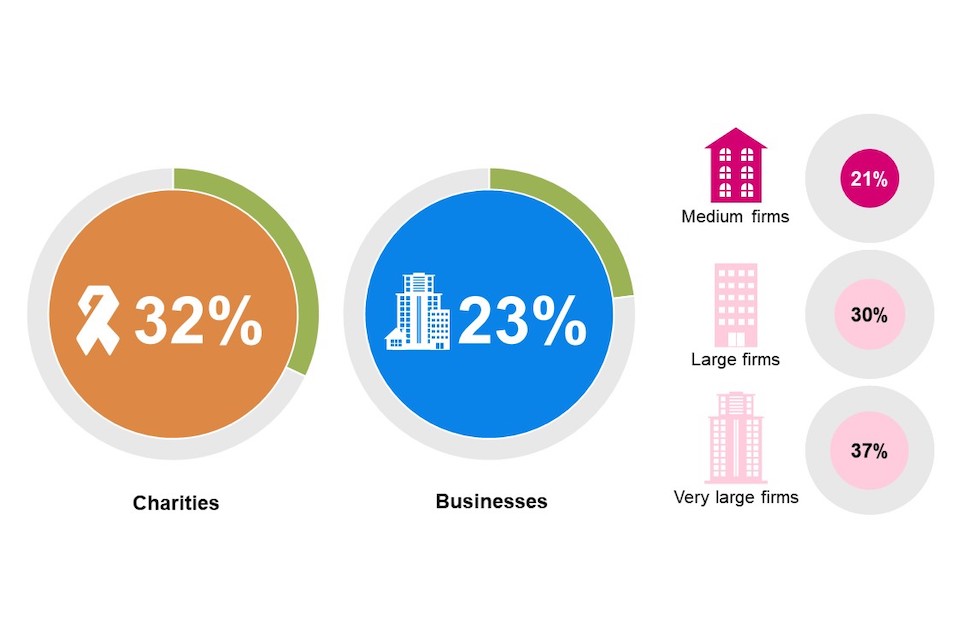

In addition to the relatively low levels of board engagement with cyber security, both businesses and charities are relatively unlikely to report that their board members have received any cyber security training.

There is a gap between the levels of board training and more general staff training on cyber security. The proportion of organisations reporting their board members had received any cyber security training is lower than the proportion offering cyber security training to their staff in the last twelve months, across both businesses (48% said they offered training to staff in the last twelve months vs. 35% saying board members had received training at any time) and charities (55% vs. 28% respectively).

Figure 3.3: Board-level cyber security training

Have any of the board received any cyber security training? (% yes)

Base: All charities (n=536), All businesses (n=1,205). Don’t know responses not shown: 21% of businesses and 22% of charities

In terms of business size, around half of very large businesses with 500+ employees (48%) report their board members have received any cyber security training, compared to one in three medium businesses (33%). By sector, businesses in finance and insurance (64%) and information and communications (61%) are the most likely to say their board members have received any cyber security training, while those in the food and hospitality sector are the least likely (25%).

Businesses and charities where the board has received any cyber security training are also more likely to report more frequent board-level discussions or updates on cyber security. For example, 64% of businesses and 61% of charities where the board has received training on cyber security also say they have board-level discussions or updates on cyber security at least monthly. This is in comparison to just 21% of businesses and 24% of charities where the board has not received cyber security training. This suggests that there is a link between the level of board members’ buy-in to cyber security issues and the levels of cyber training and discussions that take place among board members.

There is also a positive correlation between adhering to cyber security certifications or standards, and board members having received cyber security training. For example, more than half of businesses adhering to ISO 27001 (59%), the Cyber Essentials standard (57%) or the Cyber Essentials Plus standard (63%) say that their board has received cyber security training, compared to just 26% of those businesses who do not hold any of these certifications.

3.3 Attitudes to cyber risk

Businesses and charities reporting that their board has discussions or updates about cyber security were asked how they typically engage with any information on the cyber security risk the organisation faces. Around three in five such businesses (55%) and charities (60%) agree that their board integrates cyber risk considerations into wider business areas, while just over one in ten (13% of businesses and 11% of charities) disagree with this statement.

Looking specifically at businesses with boards discussing cyber security, large businesses (250+ staff) are more likely than medium businesses to agree with this statement (61% vs. 53% respectively). Additionally, businesses in the finance and insurance (70%) and information and communications (72%) sectors are the most likely to agree that their board integrates cyber risk considerations into wider business areas. In turn, those in the utilities and production (19%) and retail and wholesale (18%) sectors are the most likely to disagree.

Figure 3.4: Board engagement with cyber risk

| How much would you agree or disagree with the following statement? The board integrates cyber risk considerations into wider business areas | Strongly agree | Tend to agree | Neither agree or disagree | Tend to disagree | Strongly disagree | Don’t know | Total |

|---|---|---|---|---|---|---|---|

| Businesses | 21% | 34% | 19% | 10% | 3% | 13% | 100% |

| Charities | 20% | 40% | 20% | 10% | 2% | 8% | 100% |

Base: All whose board discusses cyber security, businesses (n=1,037), charities (n=442)

As with previous findings, there is a positive relationship between having technical controls in place in all five of the areas required to attain Cyber Essentials, adhering to cyber security standards and more board engagement. For instance, three-quarters (73%) of businesses and an even higher proportion of charities (84%) that adhere to ISO 27001 agree that their board integrates cyber risk considerations into wider business areas. [footnote 9]

Increased attention given to cyber security after an incident is experienced was a consistent theme during the qualitative interviews, with many respondents suggesting that the experience of an incident is often the only thing that incentivised or could incentivise board members to engage with cyber security more closely and integrate with wider business considerations.

Respondents also mentioned that cyber security, or more generally IT, tends to be seen more as a facilitator of the business than a strategic driver among senior leadership. Therefore, it is unlikely to be thought of in a strategic context:

“I think it [cyber security] is [included in our strategy], but it hasn’t got a line item. If we have a new solution or improvement to be made, we make sure it is secure by default. We have privacy by design. It needs to be a given. It is not a strategy in itself, but [cyber security] is something we make sure by default that is what we want it to be.”

Business, Large, Professional, scientific and technical

Chapter 4 – Sources of information

4.1 Use of NCSC guidance

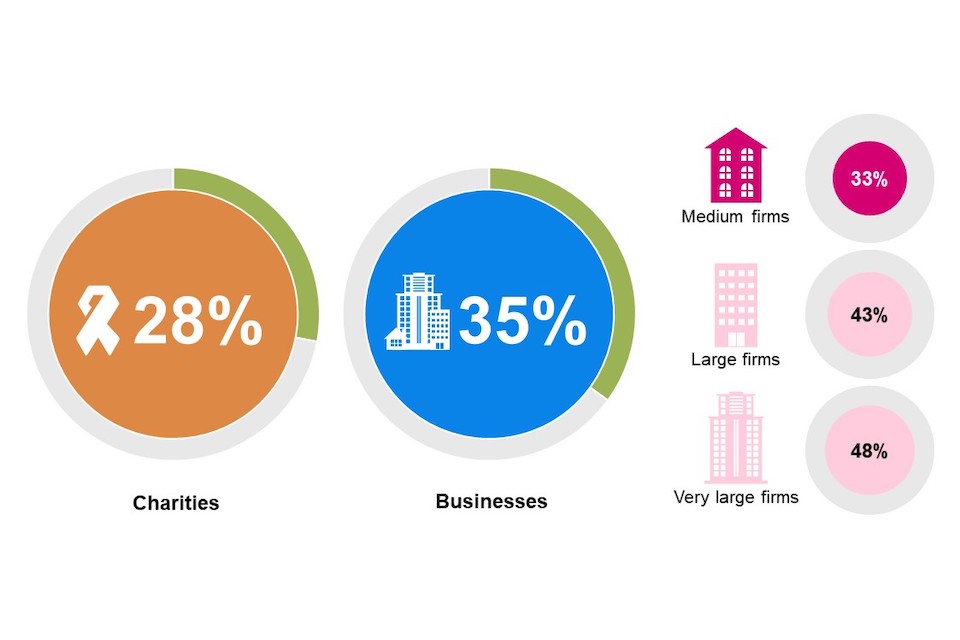

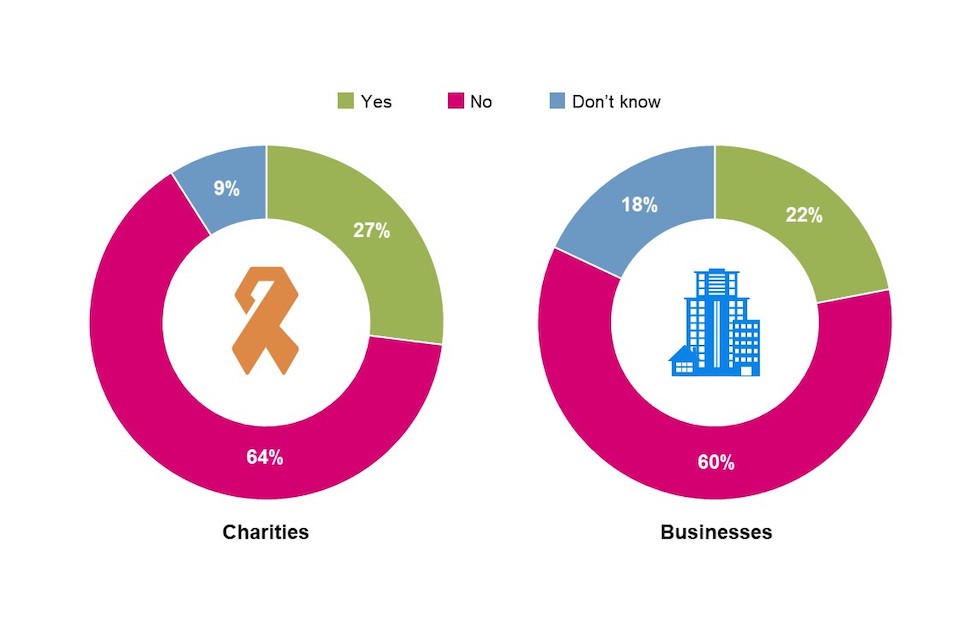

Around one-third (32%) of charities and one-quarter (23%) of businesses have used information or guidance from the National Cyber Security Centre (NCSC) in the last twelve months. However, businesses are more likely than charities to say they do not know if they have used NCSC guidance (23% vs. 16%).

Figure 4.1: Use of NCSC guidance

In the last twelve months, has your organisation used any information or guidance from the National Cyber Security Centre (NCSC) to inform your approach to cyber security? (% Yes)

Base: All businesses (n=1,205); All charities (n=536). Don’t know not shown.

Very large businesses (37%) are more likely than large businesses (30%), which are in turn more likely than medium businesses (21%), to have used NCSC information or guidance in the last year. Usage of NCSC guidance is also higher among finance and insurance (51%) and information and communications (41%) businesses.

Around half of businesses certified to the Cyber Essentials (47%) or Cyber Essentials Plus (52%) standards used NCSC information in the last twelve months, a higher proportion than those certified under ISO 27001 (37%, which is still greater than the overall average). Prevalence is also higher among businesses whose boards discuss cyber security at least monthly (40%) and businesses that experienced a cyber incident in the last twelve months compared to those that did not (28% vs. 15% respectively).

Similar differences apply among charities. Just over half of charities certified to Cyber Essentials (51%) or Cyber Essentials Plus (55%) used NCSC information in the last year. Usage of NCSC guidance is also higher in charities whose boards discuss cyber security at least quarterly (40%), and those that experienced a cyber incident in the last twelve months compared to those that did not (38% vs 20%). As many as 45% of charities reporting non-phishing incidents in this time used NCSC guidance.

Among organisations that have made use of NCSC guidance, just over half have used ‘The 10 Steps to Cyber Security’ (57% of businesses and 55% of charities), followed by the NCSC’s Cyber Assessment Framework (41% of businesses and 43% of charities).

Figure 4.2: Use of NCSC guidance (among organisations using NCSC guidance)

| Which of the following, if any, have you used? | Businesses | Charities |

|---|---|---|

| The 10 steps to Cyber Security | 57% | 55% |

| NCSC’s Cyber Assessment Framework | 41% | 43% |

| NCSC guidance on secure home working or video conferencing | 33% | 40% |

| NCSC weekly threat reports | 32% | 30% |

| The Cyber Security Board Toolkit | 23% | 24% |

| NCSC guidance for moving your business online | 10% | 12% |

| Any | 81% | 86% |

Base: All who used NCSC information or guidance in the last twelve months; Businesses (n=311); Charities (n=169). Don’t know/ none of these not shown.

In the qualitative research, several participants mentioned that they had found the NCSC a useful source of information. Specific examples of this were sharing NCSC posters and guidance with staff to raise awareness of cyber security and implementing guidance on sharing passwords and regular alerts:

“I’ve got a whole folder of bookmarked pages from them [the NCSC website] that I find especially useful.”

Business, Medium, Information and communications

4.2 Other information sources/influencers

A crucial factor in strengthening UK cyber resilience is understanding how best to positively influence organisations to take action and improve their cyber defences. The survey highlights that, of the six groups asked about, the greatest external influence in the last twelve months has come from external cyber security consultants. Around half of businesses (47%) and charities (55%) say that feedback from external IT or cyber security consultants influenced their actions on cyber security.

Fewer organisations report being influenced by insurers (26% for businesses and 30% for charities), regulators (21% and 27% respectively), and auditors (19% and 21% respectively). Among businesses, 21% report being influenced by customers, and 12% by investors or shareholders in the last year. Charities are more likely than businesses to have been influenced by external consultants and regulators.

Figure 4.3: Influence of external sources on actions

| Over the last twelve months, how much have your actions on cyber security been influenced by feedback from any of the following groups? | Businesses | Charities |

|---|---|---|

| External IT or cyber security consultants | 47% | 55% |

| Your insurers | 26% | 30% |

| Regulators for your sector | 21% | 27% |

| Your customers* | 21% | 0% |

| Whoever audits your accounts | 19% | 21% |

| Any investors or shareholders* | 12% | 0% |

Base: All businesses (n=1,205); All charities (n=536). Showing Net: A great deal/fair amount only. *Please note, charities were not asked if they had been influenced by feedback from their customers or investors/ shareholders as these options are not relevant to charitable organisations.

Very large businesses with 500+ employees are more likely than average to mention auditors (28%) and are also more likely than medium sized businesses to say they have been influenced by regulators (27% vs. 20%) and investors (19% vs. 11%). Large businesses with 250+ employees are more likely than medium sized businesses to have been influenced by insurers (32% vs. 25%).

Patterns of influence differ by sector:

- External IT or cyber security consultants are more likely to be mentioned by finance and insurance (64%) businesses

- Finance and insurance (67%), information and communications (37%) and health, social care and social work (33%) businesses are more likely than average to have been influenced by regulators

- Customers are more likely to have influenced businesses in the information and communications (45%) and transport and storage (28%) sectors

- Investors or shareholders are more likely to be sources of influence for finance and insurance (25%), information and communications (also 25%) and transport and storage (20%) businesses

In general, organisations with certifications, with boards that discuss cyber security at least monthly, and which experienced a cyber incident in the last twelve months, are more likely to say they are influenced by each of the stakeholders mentioned in the survey.

Charities (20%) are more likely than businesses (14%) overall to have reviewed or changed any of their cyber security policies or processes because of an organisation in their sector experiencing a cyber security incident. Charities are also more likely than businesses (14% vs. 10%) to have acted because of another organisation in their sector implementing similar measures.

Large businesses (250+ staff) are more likely than medium businesses to have reviewed or amended their policies because of an organisation in their sector experiencing a cyber incident (24% vs. 12% respectively) or implementing similar measures (17% vs. 9% respectively). The likelihood of both is also greater among organisations with boards that discuss cyber security at least monthly, that have cyber security certifications, and which have experienced a cyber incident in the last twelve months. Businesses in the information and communications sector (20%) are more likely than businesses on average to have reviewed or changed their cyber security policies or processes because of another organisation in their sector implementing similar measures.

The qualitative research found that some organisations fully depend on their IT consultants to keep them up to date with any actions required on cyber security. There is typically a high degree of trust in this relationship, though services could also be switched between contractors for a fresh perspective. For other organisations, suppliers have a more informative role, providing them with updates and alerts that they can then choose how to action:

“I do my best to keep in touch with the whole field. I subscribe to all the vulnerability stuff that comes through from the vendors we use. The Microsoft security centre blogs. A lot of it is keeping your ear to the ground internet-wise and you can pick up a lot of what is going on.”

Charity

Chapter 5 – Cyber security policies

This section discusses the cyber security policies organisations have in place, including documentation, cyber insurance policies and staff training.

5.1 Governance and planning

The survey asked about five types of documentation that organisations may have in place as part of an effective cyber security strategy. This included: a Business Continuity Plan covering cyber security, documentation identifying critical assets, documentation about the IT estate and vulnerabilities, a risk register covering cyber security, and documentation on the organisation’s ‘risk appetite’ (i.e., the level of cyber risk the organisation is willing to accept).

Of the five different types of documentation tested that help organisations manage cyber security risks, having a Business Continuity Plan that covers cyber security is the most common across both businesses and charities (69% and 73% respectively). Of the types of documents tested, both businesses (26%) and charities (31%) are least likely to have documentation that outlines how much cyber risk the organisation is willing to accept. More than half of organisations say they have documentation that identifies the most critical assets that the organisation wants to protect (56% of businesses and 60% of charities), and a written list of the organisation’s IT estate and vulnerabilities (54% of businesses and 58% of charities). Having a risk register that covers cyber security in place is much more common among charities than businesses, with seven in ten (71%) charities saying they have this compared to just under half (48%) of businesses.

Figure 5.1: Documentation in place to manage cyber security risks

| Does your organisation have any of the following documentation in place to help manage cyber security risks? | Businesses | Charities |

|---|---|---|

| A Business Continuity Plan that covers cyber security | 69% | 73% |

| Any documentation that identifies the most critical assets that your organisation wants to protect | 56% | 60% |

| A written list of your organisation’s IT estate and vulnerabilities | 54% | 58% |

| A risk register that covers cyber security | 48% | 71% |

| Any documentation that outlines how much cyber risk your organisation is willing to accept | 26% | 31% |

Base: All businesses (n=1,205); All charities (n=536). Don’t know not shown.

Overall, fewer than one in five organisations say they have all five types of documentation in place to manage cyber security risk (17% both for businesses and charities). Businesses are more than twice as likely as charities to say they have none of these documents (18% vs. 8% respectively).

Large businesses (250+ staff) are more likely than medium businesses to report having all five documents (21% vs. 16% respectively), while medium businesses are more likely than large businesses to say they have none (19% vs. 12% respectively). Having all five types of documentation is most common among businesses in the information and communications (35%) and finance and insurance (34%) sectors. In contrast, businesses in the food and hospitality (28%) and retail and wholesale (25%) sectors are the most likely to say they have none of the documents in place.

During the qualitative interviews these processes were further explored, particularly focusing on incident response plans which are discussed in more detail in section 6 of this report. Whether organisations had a written incident response plan varied from relying completely on external IT suppliers to having processes in place adhering to ISO standards. In line with the quantitative findings, respondents from large businesses were the most likely to report having sophisticated cyber security policies and processes in place, including robust, ISO 27001 compliant incident response plans. Respondents adhering to standards and certifications suggested that the periodic testing required by these helped to reinforce governance and planning more generally.

5.2 Cyber insurance policies

Having some form of cyber insurance cover is relatively common among organisations. Charities are more likely than businesses to report they have some form of cyber insurance (66% vs. 53% respectively). However, at least some of this difference is explained by more business respondents than charity respondents saying that they do not know their organisation’s cyber insurance status (34% vs. 20% respectively). Among businesses, 57% of both large (250-499 staff) and very large (500+ staff) businesses say they have some form of cyber insurance.

Figure 5.2: Organisations with cyber insurance

| Which of the following best describes your situation? | Businesses | Charities |

|---|---|---|

| Have a cyber insurance policy | 53% | 66% |

| Don’t have a cyber insurance policy | 13% | 14% |

| Don’t know | 34% | 20% |

Base: All businesses (n=1,205); All charities (n=536).

Regarding the type of cover held, businesses and charities are both more likely to have cyber security cover as part of a broader insurance policy than having a specific cyber insurance policy. Having a specific cyber security insurance policy is more common among charities than businesses, with one-quarter of charities having this type of cover compared to fewer than one in five businesses (24% vs. 18% respectively).

While one-quarter of large businesses (250+ staff) (24%) report having a specific policy, only 17% of medium businesses say the same. One in three businesses in the finance and insurance sector (34%), and close to three in ten (28%) businesses in the information and communication sector, say they have a specific cyber insurance policy. This compares to 9% of businesses in the health and social care sector.

Figure 5.3: Type of cyber insurance policy organisations have

| Which of the following best describes your situation? | Businesses | Charities |

|---|---|---|

| We have cyber security cover as part of a broader insurance policy | 35% | 42% |

| We have a specific cyber security insurance policy | 18% | 24% |

| We are not insured against cyber security incidents | 13% | 14% |

Base: All businesses (n=1,205); All charities (n=536). Don’t know not shown.

5.3 Staff training

When asked about whether they carried out any cyber security training or awareness raising sessions in the last twelve months specifically for any staff/staff or volunteers who are not directly involved in cyber security, charities are more likely than businesses to say they did (55% vs. 48%), although this varied by business size and sector. While just under half (45%) of medium businesses say they carried out such training, six in ten (60%) large businesses (250+ staff) say they did. However, looking at large businesses in more detail, businesses with 500+ staff were much more likely than those with 250-499 staff to say they had carried out cyber security training in the last year (70% vs. 51%).

Around eight in ten businesses in the finance and insurance (79%) and information and communications (78%) sectors say they had offered training to staff in the last twelve months, compared to around just one in three businesses in the food or hospitality (31%), construction (35%) or health, social care and social work (also 35%) sectors.

Respondents during the qualitative interviews were asked whether their organisation had conducted a cyber skills assessment of their workforce. Most respondents had limited understanding of what this might cover and some thought of it as interchangeable with offering training:

“Something else to do! Is there a standard one around?”

Business, Medium, Construction

Among those familiar with the concept, a common view among charity respondents was that conducting a cyber skills assessment of their workforce would have little to no value, citing either that staff members tend to only use email, or assuming high level of IT illiteracy among staff. Among businesses, those that did some form of skills assessment referred to sending out fake phishing emails and testing the likelihood of reporting these.

Chapter 6 – Cyber security processes

This section discusses the cyber security processes businesses and charities have in place, including any standards and certifications held, as well as the monitoring and evaluation of their policies where relevant and any improvements made over the last twelve months.

6.1 Standards and certifications

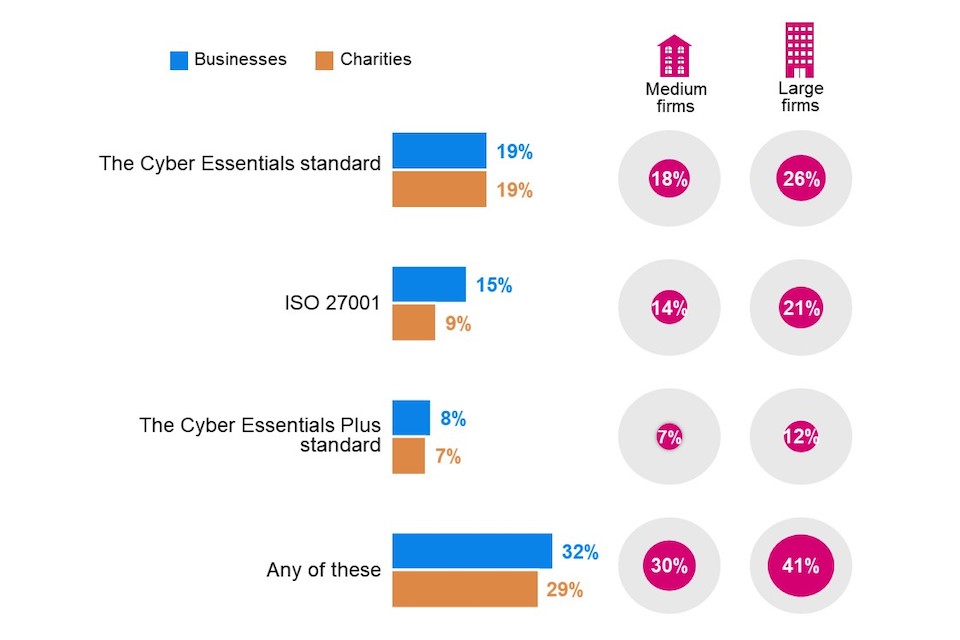

Around three in ten businesses (32%) and charities (29%) report having one or more of the three cyber security certifications asked about. The most common certification adhered to by businesses and charities (19% of both) is Cyber Essentials,[footnote 10] followed by ISO 27001, [footnote 11] which is more common among businesses (15%) than charities (9%). Cyber Essentials Plus[footnote 12] is less common, at eight per cent among businesses and seven per cent among charities. Around two-fifths (41% of businesses and 46% of charities) have none of the three certifications asked about, and a further quarter (26% of businesses and 25% of charities) say they do not know.

Figure 6.1: Standards or certifications adhered to by organisations

Base: All businesses (n=1,205); All charities (n=536). Don’t know not shown.

Large businesses and businesses with boards that discuss cyber security at least monthly are more likely than businesses on average to have each of the three certifications.

There are some clear differences by sector:

- Businesses in the information and communications sector are more likely than businesses on average to have each of the three certifications. Almost half (47%) have ISO 27001, 42% are certified with Cyber Essentials and 27% have Cyber Essentials Plus.

- Finance and insurance sector businesses are more likely than businesses on average to hold Cyber Essentials (32%) and Cyber Essentials Plus (17%) certification, as are those in the professional, scientific and technical sector (31% and 15% respectively).

- Administration and real estate sector businesses are more likely than businesses on average to have ISO 27001 (21%).

- Businesses in the following sectors are more likely than average to have none of these three certifications, or not to know if they do: food and hospitality; health, social care and social work; retail and wholesale; and utilities and production.

Businesses that experienced a cyber incident in the last twelve months are more likely to have Cyber Essentials (22% vs. 15% of those that have not experienced an incident) and Cyber Essentials Plus (9% vs. 6%).

The qualitative research identified three different triggers for becoming certified. The reason mentioned most often by participants is that certifications are increasingly becoming a contractual requirement for working with public sector bodies and large companies.

“It became obvious that if we wanted to continue working with these people, we should get ISO 27001 accreditation. [Cyber Essentials] doesn’t offer any more than what we get from ISO 27001, but certain things say you have to have Cyber Essentials, so we have that as well.”

Business, Large, Administration and real estate

The other two drivers were a change in senior personnel, such as a new Chief Financial Officer (CFO) and having a new IT supplier. This could lead to organisations reviewing their whole approach to cyber security and deciding to become certified. Some of these participants felt that the process of obtaining a certification enabled their organisation to examine and improve their cyber security.

“It opened our eyes a bit. It allowed us to explore our security across many different assets. We had some of this in place, but it probably wasn’t where it should have been. Getting that Cyber Essentials Plus in place allowed us to have that investment and spend it wisely on some of the areas that we felt there were gaps. It was difficult, but we passed it.”

Business, Large, Professional, scientific and technical

6.2 Processes currently in place

The overwhelming majority of organisations say that they have various rules and controls already in place, with more than nine in ten organisations reporting that they have the following technical controls required to attain Cyber Essentials in place:

- 96% of both businesses and charities say they restrict IT admin and access rights to specific users

- 95% of businesses and 96% of charities have up-to-date malware protection across all their devices

- 94% of businesses and 92% of charities have firewalls that cover their entire IT network, as well as individual devices

- 92% of businesses and 94% of charities have security controls on their organisation’s own devices.

More than six in ten organisations (63% of businesses and 61% of charities) report having a policy to apply software security updates within 14 days.

Overall, more than half of businesses and charities (57% of each) have technical controls in place in all five of the areas required to attain Cyber Essentials. In addition, nearly two in three organisations (66% of businesses and 64% of charities) say they monitor user activity, while the vast majority of businesses (85%) and charities (87%) have specific rules for storing and moving files containing people’s personal data.

Businesses are more likely than charities to back up data securely via a non-cloud service (70% vs. 64%), though usage of cloud services for secure data backup is similar (74% of businesses and 77% of charities). Large businesses (250+ staff) are more likely than medium businesses to have specific rules for storing and moving files containing people’s personal data (89% vs. 84%).

Figure 6.2: Technical controls in place in the areas required to attain Cyber Essentials

| And which of the following rules or controls, if any, do you have in place? | Businesses | Charities |

|---|---|---|

| IT admin/ access rights | 96% | 96% |

| Malware protection | 95% | 96% |

| Network firewalls | 94% | 92% |

| Security controls | 92% | 94% |

| Patch management | 63% | 61% |

| Have all five technical controls in place required to attain Cyber Essentials | 57% | 57% |

Base: All businesses (n=1,205); All charities (n=536). Don’t know not shown.

Large businesses and medium businesses are similarly likely to have technical controls in place in each of five of the areas required to attain Cyber Essentials, except for restricting IT admin/access rights, which is more prevalent among large businesses (99% vs. 95% of medium businesses). There is also little difference between businesses and charities on these measures.

Businesses in certain industry sectors are more likely than average to have technical controls in place in all five of the areas required to attain Cyber Essentials: financial and insurance (76%), information and communications (71%), and professional, scientific or technical (also 71%). Businesses that have experienced a cyber security incident in the last twelve months, and those experiencing an impact from such an incident, are also more likely to have technical controls in place in all five of the areas required to attain Cyber Essentials (62% of both groups, compared to 57% of all businesses). This pattern also emerged in the qualitative interviews where businesses that relied more heavily on digital technologies were more likely to have invested in the technical controls required to attain Cyber Essentials. For example, one transport business whose core business is less reliant on digital technology and had started as a farming business explained:

“You’ve still got that same person who is a farmer and doesn’t like the look of any technology or computer. We’re still trying to catch up on technological systems in filing and sharing information. Trying to change the culture of the business is difficult because of the people who are leading it, who are still in that old-school mind.”

Business, Medium, Transport and storage

In addition, businesses whose board are informed more frequently on cyber security are more likely to have technical controls in place in all five of the areas required to attain Cyber Essentials (68% whose board receives at least monthly updates and 65% whose board receive at least quarterly updates, compared to 36% of those whose board never receive updates). This difference is also observed among charities, with 85% of charities whose board receives at least monthly cyber security updates having technical controls in place in all five of the areas required to attain Cyber Essentials, compared with just 34% of charities whose board never receive any cyber security updates.

Businesses that experienced a cyber incident in the last twelve months are also more likely to have technical controls in place in all five of the areas required to attain Cyber Essentials (62% vs. 50% of businesses not reporting an incident). This was supported by the qualitative interviews, where businesses explained that investment in cyber security is often triggered by an incident:

“It is not the priority. You rely on these things, and you don’t take a second thought on it until it goes wrong. That is an issue for us as a business. It is not a priority that is discussed enough, only when something really goes wrong”.

Business, Medium, Transport and storage

The qualitative interviews provided insight into how much of a driver acquiring cyber security certifications can be for establishing more robust security practices and embedding them across their organisations.

“The requirement to be Cyber Essentials Plus certified started a programme of work. It opened our eyes a bit. It allowed us to explore our security systems from across many different aspects: patching of systems, making sure our mobile devices are of a particular standard and making sure we are aware of all vulnerabilities across our servers, desktops and laptops. And also training… getting that Cyber Essentials Plus in place allowed us to have that investment and spend it wisely on some of the areas that we felt there were gaps.”

Business, Large, Professional, scientific and technical

The qualitative interviews also provided insight into the motivation for acquiring certifications. Several businesses explained that it was a necessity to be able to bid for contracts with large public sector clients. Without this requirement, some businesses would not have invested to the same extent in cyber security because of the level of investment needed and concerns over whether the investment would be proportionate to the financial gains. Businesses pursuing Cyber Essentials certification to meet client procurement standards were positive about this requirement.

“We are driven quite heavily by [Regulator], which does actually make us better. They drive us down the cyber security route, it means you don’t forget to do things. It is quite useful to have a demanding client like that”.

Business, Medium, Construction

6.3 Monitoring and evaluation

Annual reports

Overall, charities are more likely than businesses to state that cyber security was included in their organisation’s most recent annual report (18% vs. 14%). Large businesses with 250+ employees are more likely than medium businesses to have included cyber security in their annual report (18% compared to 13%).

Around half of organisations say cyber security was not included in their organisation’s most recent annual report, with this applying to more charities than businesses (57% vs. 45%). However, businesses are more likely than charities not to know whether their annual report mentions anything about cyber security (34% vs. 23%). This was supported by the qualitative interviews, where uncertainty was observed about the detail of what is and is not covered in annual reports.

Figure 6.3: Reporting on Cyber Security

| Did you include anything about cyber security in your organisation’s most recent annual report? | Yes | No | Don’t know | Not applicable / don’t have annual reports | Total |

|---|---|---|---|---|---|

| Businesses | 14% | 45% | 34% | 7% | 100% |

| Charities | 18% | 57% | 23% | 2% | 100% |

Base: All businesses (n=1,205); All charities (n=536).

There is a link between how engaged senior leadership is with cyber security issues and whether annual reports include anything about cyber security. Organisations with a board that receive regular information or updates about cyber security are more likely to include cyber security in their most recent annual report, with 25% of businesses and 36% of charities whose board receives updates on cyber security at least monthly reporting that cyber security was included in their last annual report.

Businesses in the information and communication sector (24%), construction (also 24%), and finance and insurance sector (23%) are the most likely to have included anything about cyber security in their annual reports. During the qualitative interviews, several businesses indicated that their annual reports are typically aimed at shareholders, with a high-level view of performance measures and profitability. An in-depth look at key risks, such as cyber security, often does not fall into the scope of these reports. Charities discussed how their annual reports tend to focus on their main projects throughout the year and their main achievements, and therefore things like cyber security are not included because it would not fit the tone of the report.

“We tend to use our annual report more as a celebration of the kind of support we’ve offered to the community, so it doesn’t fit particularly well with the tone of what we do.”

Charity

The qualitative interviews also provided more insight into the type of detail that is covered in annual reports among the minority of organisations who do include coverage of cyber security. A number of organisations, both charities and businesses, suggested that cyber security might be covered in their annual report but under a larger section on digital infrastructure or as part of the risk register.

Identification of cyber security risks

Having procedures in place to monitor and identify cyber security risks is crucial to make sure the correct systems are in place to deal with these risks. The vast majority of businesses and charities have taken at least one action in the last twelve months to identify such risks.

Conducting a risk assessment covering cyber security risks is the most commonly reported action, with charities more likely than businesses to have done this (73% vs. 65%). This is followed by having used specific tools designed for security monitoring (61% both of businesses and charities). Around half have completed a cyber security vulnerability audit (47% of businesses and 50% of charities), while around three in ten (34% of businesses and 31% of charities) have invested in threat intelligence.

Overall, businesses are more likely than charities to report not taking any of the four actions covered in Figure 6.3 (18% vs. 13%).