Operation of the subsidy control functions of the Subsidy Advice Unit

Published 11 November 2022

© Crown copyright 2022

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: [email protected].

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/guidance-on-the-operation-of-the-subsidy-control-functions-of-the-subsidy-advice-unit/operation-of-the-subsidy-control-functions-of-the-subsidy-advice-unit

Introduction

Purpose and scope of the Guidance

This guidance document explains how the Subsidy Advice Unit (SAU[footnote 1]), which is part of the Competition and Markets Authority (CMA[footnote 2]), will exercise its functions under the Subsidy Control Act 2022 (the ‘Act’).

The purpose of this document is to:

- guide those seeking information on the subsidy control functions of the SAU, and the associated timescales and procedures

- explain how the SAU will discharge its functions set out in the Act, including some of the technical concepts and analytical approaches involved, and our approach to prioritising cases

Structure of this Guidance

| The Introduction explains the scope and purpose of this guidance including the role of the CMA and the SAU in the Act. | Who is this document for? What other guidance and frameworks exist? What is the SAU and what functions does it perform? |

| Chapter 2 Overview of the Subsidy Advice Unit’s functions outlines the powers and functions of the SAU, including its information-gathering powers. | Why do subsidies need to be referred to the SAU? What is the difference between mandatory and voluntary referrals? How long does a referral take? What are the SAU’s monitoring duties? How will the SAU gather information? |

| Chapter 3 Procedural arrangements sets out the procedures for requesting advice from the SAU and the key processes it will use. | How to submit a request for a report to the SAU. How should Public Authorities and Third Parties engage with the SAU? What transparency information will be available? How will confidential information be protected? |

| Chapter 4 Analytical framework outlines the analytical approach that the SAU will adopt in discharging its functions. | What are the Subsidy Control Principles and Energy and Environment Principles? What analysis will the SAU perform during its evaluation? What supporting evidence may be included in the referral? What will the SAU’s reports contain? |

| Chapter 5 Prioritisation principles sets out the prioritisation principles which outline the factors the SAU may consider whether to produce a report following a voluntary referral. | Why might the SAU reject a voluntary referral? What might a Public Authority need to discuss with the SAU before submitting a voluntary referral? |

| Glossary | A glossary is provided which defines some key terms which are identified in bold text throughout the document. |

| Annex A: Submission of supporting documents in a request for a report | What is the format and structure for submitting a request for referral to the SAU? How should confidential information be identified in the request? |

| Annex B: 4-Step framework and the Subsidy Control Principles | How do the Subsidy control principles map against the four-step framework presented in the Analytical Framework Chapter? What questions will the SAU ask when assessing each of the 4 steps? |

This guidance should be read alongside the Act as well as regulations and guidance to be adopted by the Secretary of State[footnote 3] under the Act, including but not limited to:

- the Statutory Guidance for the United Kingdom Subsidy Control Regime issued by the Secretary of State (‘BEIS Statutory Guidance’[footnote 4])[footnote 5]

- the Subsidy Control (Subsidies and Schemes of Interest of Particular Interest) Regulations 2022[footnote 6]

- any regulations on the information that must be included in a public authority’s entry in the Subsidy Database[footnote 7] in relation to a subsidy or subsidy scheme[footnote 8]

This guidance should also be read alongside the Statement of Policy on the Enforcement of the SAU’s Information Gathering Powers, which will be published in autumn 2022.[footnote 9]

References to ‘subsidies’ in this document should generally be considered as applying to both subsidies and subsidy schemes.[footnote 10]

The SAU will apply this guidance flexibly. This means that the SAU will have regard to this guidance when considering referrals from public authorities and when preparing its reports but that the SAU may take a different approach when the facts of the case justify doing so. At the time of publication of this Guidance, the Act has not been commenced fully and the SAU has not been established as a committee of the CMA Board. It is anticipated that the Guidance will be adopted formally by the SAU in due course.

This document is not a definitive statement of, or substitute for, the law itself. Stakeholders should refer to the relevant legislation and guidance and, if necessary, seek independent legal advice.

We will keep this guidance under review, and we expect to update it to reflect changes in best practice and the law.

The SAU

The Subsidy Advice Unit is part of the CMA and will be responsible for discharging the CMA’s functions and powers under Part 4 of the Act. This document uses the term SAU when referring to the CMA fulfilling its subsidy control functions.

Through its review and monitoring functions, the SAU will support public authorities’ decision making regarding the design and assessment of subsidies to help ensure that they are based on a strong assessment of their compliance with the Subsidy Control Requirements[footnote 11] (Assessment of Compliance[footnote 12]).

The SAU will provide advice in respect of certain subsidies or subsidy schemes (known as subsidies or schemes of interest and subsidies or subsidy schemes of particular interest (SSoI[footnote 13]) and (SSoPI[footnote 14])) that public authorities refer to it, evaluating their Assessment of Compliance with the requirements of the Act. The SAU’s advice to public authorities will be non-binding, with public authorities responsible for deciding whether to award a subsidy or make a scheme.

The SAU will also monitor and report on the effectiveness of the operation of the Act, and its impact on competition and investment within the UK.

Overview of the Subsidy Advice Unit’s functions

What this chapter does

This chapter provides an outline of the SAU’s functions and powers,[footnote 15] as well as a brief description of how the SAU will gather information in carrying out its work.

The Subsidy Advice Unit’s functions

As described in more detail below (visit What the SAU is required to do section), the SAU’s functions fall under the following two categories:

- providing independent advice to public authorities in relation to certain subsidies which are referred to the SAU. This advice will take the form of an evaluation of the referring public authorities’ Assessment of Compliance. Those requirements include the subsidies’ compliance with the subsidy control principles[footnote 16] (the Principles) and, where applicable, the energy and environment principles[footnote 17] (the E&E Principles).[footnote 18] Public authorities are required to refer to the SAU SSoPIs or subsidies called-in by the Secretary of State[footnote 19] (i.e. mandatory referral). The SAU also has a discretion to provide such advice in relation to any SSoIs which are referred to it on a voluntary basis (i.e. voluntary referral).[footnote 20] The Secretary of State also has the power to refer a subsidy or scheme to the SAU post-award in certain circumstances (i.e. ‘post-award referrals’)[footnote 21]

- monitoring and reporting on the effectiveness of the operation of the Act and its impact on competition and investment within the United Kingdom

The SAU will not decide whether a subsidy can be given, or directly assess whether it complies with the Subsidy Control Requirements. Public authorities are responsible for taking decisions about subsidies, based on their own Assessment of Compliance, having the benefit of the SAU’s evaluation.[footnote 22]

The Subsidy Control Requirements and Exempt Subsidies

This section provides an overview of certain provisions of Act which are relevant to the SAU’s functions.[footnote 23] Further information on these is available in BEIS Statutory Guidance.[footnote 24]

The Subsidy Control Requirements

Before giving a subsidy or making a subsidy scheme, public authorities must consider the Principles. They must not give the subsidy or make the scheme unless they are of the view that the subsidy or scheme is consistent with the Principles.[footnote 25]

In addition, and as described in more detail in the BEIS Statutory Guidance, there are certain categories of subsidies which are permitted if particular requirements are fulfilled,[footnote 26] namely:

- subsidies for the relocation of activities[footnote 27]

- subsidies for rescuing or restructuring ailing or insolvent enterprises[footnote 28]

- subsidies for insurers that provide export credit insurance[footnote 29]

- subsidies for air carriers for the operation of routes[footnote 30]

- subsidies for the purpose of providing services of public economic interest (SPEI)[footnote 31]

The Act identifies certain categories of subsidies which are generally prohibited and so cannot be granted by public authorities.[footnote 32] The SAU does not have a role in enforcing rules relating to prohibited subsidies. However, prohibited subsidies can be challenged in the courts by an interested party.[footnote 33]

Exempt subsidies

The requirement to apply the Subsidy Control Requirements in their entirety does not apply in relation to a category of ‘exempt’ subsidies.[footnote 34]

In particular, the Subsidy Control Requirements do not apply to subsidies to compensate for damage caused by natural disasters and other exceptional circumstances. There is also a limited application of the Subsidy Control Requirements to subsidies given on a temporary basis in response to national or global economic emergencies.[footnote 35]

Additional miscellaneous exemptions apply in the areas of:[footnote 36]

- National security [footnote 37]

- Bank of England monetary policy [footnote 38]

- Financial stability [footnote 39]

- Legacy and withdrawal agreement subsidies [footnote 40]

- Tax measures [footnote 41]

- Large cross-border or international cooperation agreements[footnote 42]

- Nuclear energy [footnote 43]

Further information on exempt subsidies is available in BEIS Statutory Guidance.[footnote 44]

What the SAU is required to do

This section explains the SAU’s functions of (i) preparing and publishing reports on assessments of subsidies and schemes which are referred to it, and (ii) monitoring and reporting on the effectiveness of the operation of the Act and the impact of its operation on competition and investment within the United Kingdom.[footnote 45]

Reports on referral

Mandatory referral

A subsidy must be referred to the SAU if it is an SSoPI or if the Secretary of State directs that a proposed subsidy or scheme be ‘called-in’.[footnote 46] Public authorities should refer to BEIS Statutory Guidance in determining whether a subsidy is a SSoPI (or an SSoI).

Mandatory referral requests must include at a minimum the following information:[footnote 47]

- an explanation of why the public authority considers that the subsidy or subsidy scheme would meet the definition of an SSoPI[footnote 48]

- the Assessment of Compliance the public authority conducted on the subsidy or scheme’s compliance with the Subsidy Control Requirements and the public authority’s reasons for reaching that conclusion

- any evidence relevant to making that assessment

- all of the information that the public authority would be required to upload to the subsidy database [footnote 49]

On receipt of a referral request, the SAU will assess whether the request contains the information that the referring public authority is required to provide. Within five working days (beginning on the date the request is received), the SAU will inform the public authority as to whether the required information has been provided.[footnote 50]

In circumstances where the SAU informs the public authority that the request does not meet the necessary information requirements, the public authority may submit a new request once it has addressed the deficiencies identified by the SAU.[footnote 51] In the absence of the submission of a new request, the public authority must not give the subsidy or make the scheme.

Once the SAU has accepted that the required information has been provided, a 30 working day ‘reporting period’[footnote 52] will start beginning on the date on which notice is given to the public authority that the request complies with the requirement to provide certain minimum information (see above).[footnote 53] Before the end of the reporting period, the SAU will publish a report on the referred subsidy. The report will include an evaluation of the public authority’s Assessment of Compliance, which will take into account any effects of the proposed subsidy or scheme on competition or investment within the United Kingdom. The report may also include advice about how the public authority’s assessment might be improved or the proposed subsidy may be modified to ensure compliance with the Subsidy Control Requirements.[footnote 54]

The SAU and the referring public authority can agree to extend the duration of the reporting period arising from mandatory referral.[footnote 55] In such circumstances, the SAU will publish a notice explaining that the reporting period has been extended, the length of the extension,[footnote 56] and the reasons for the extension. In exceptional circumstances, the reporting period may also be extended by the Secretary of State (up to a maximum of 40 working days beginning on the date the reporting period would otherwise have ended) in response to a request in writing to do so from the SAU.[footnote 57]

The referring public authority may not give a subsidy until a ‘cooling off’ period[footnote 58] of five working days, beginning on the day after the SAU issues its report, has elapsed.[footnote 59] The Secretary of State may extend the duration of the cooling off period (up to a maximum of 30 working days beginning on the date the cooling off period would otherwise end) if the SAU has identified in its report serious deficiencies in the public authority’s Assessment of Compliance.[footnote 60]

Voluntary referral

Public authorities are not required to refer SSoIs to the SAU, but they can choose to do so.[footnote 61] BEIS Statutory Guidance lists factors which indicate when it might be appropriate to refer an SSoI to the SAU.[footnote 62]

The information which public authorities are required to submit on making a voluntary referral is the same as that which applies in the case of mandatory referrals (visit Mandatory referal section), except that the referring public authority should explain why the subsidy or scheme in question is an SSoI, rather than an SSoPI.[footnote 63]

The SAU will have discretion in deciding whether to prepare a report following a voluntary referral. In making its decision, the SAU will have regard to its Prioritisation Principles.[footnote 64]

Within five working days (beginning on the date that the request is sent), the SAU will inform the public authority by notice either that the SAU will proceed to prepare a report on the request or, alternatively, it will provide reasons why it has decided not to prepare a report.[footnote 65]

Once the SAU has accepted the request, a reporting period of 30 working days will start (beginning on the date notice is given to the public authority) unless another period has been agreed in writing between the SAU and the public authority.[footnote 66] Before the end of the reporting period, a report must be published, in line with the report described above. The reporting period may be extended by agreement in writing between the SAU and the referring public authority.[footnote 67] In circumstances where the reporting period is either agreed or extended, the SAU will publish a notice setting out the agreement or extension and the reasons for it.[footnote 68]

Given the voluntary nature of an SSoI referral, there is no requirement for the referring public authority to observe a ‘cooling-off’ period following the SAU reporting period, and the public authority can give the subsidy before the SAU has published its report (or the reporting period has elapsed). A referring public authority should inform the SAU as soon as possible if it gives the subsidy or makes the scheme in question before the SAU has prepared or published its report. In such circumstances, the SAU will decide whether to proceed with the preparation and the publication of the report.[footnote 69]

Where a voluntary referral request has been accepted by the SAU, but the report has not yet been published and the reporting period has not yet expired, the request will be treated as a mandatory referral if the Secretary of State makes a call-in direction in relation to the subsidy in question.[footnote 70] In circumstances where the reporting period has expired, but the report has not been published, the request will be treated as a mandatory referral except that the reporting period will be a period of 10 working days, rather than 30 working days.[footnote 71]

Where a call-in direction is made by the Secretary of State after publication of the report but before the subsidy is given, a cooling off period of five working days will apply, beginning on the day after the day on which the report was published.[footnote 72] As in the case of a cooling off period following a mandatory referral, the duration of the cooling off period may be extended up to a maximum 30 working day period where the Secretary of State considers that the report has identified serious deficiencies in the public authority’s assessment of the subsidy or scheme’s compliance with the Subsidy Control Requirements.

SAU report following mandatory or voluntary referral

Before the end of the reporting period, the SAU will publish a report which will include an evaluation of the public authority’s Assessment of Compliance.[footnote 73] The SAU’s evaluation will take into account any effects of the proposed subsidy on competition or investment within the UK.[footnote 74] The SAU may also include in its report advice about how the public authority might improve its assessment and advice about how the proposed subsidy might be modified to ensure compliance with the Subsidy Control Requirements.[footnote 75]

Post-award referral

The Secretary of State may refer a subsidy or scheme to the SAU after it has been made, where the Secretary of State considers either that there has (or may have) been a failure to comply with the Subsidy Control Requirements or that there is a risk of negative effects on competition or investment in the United Kingdom.[footnote 76]

In making such a referral, the Secretary of State will at the same time direct the public authority to provide the following information to the SAU:

- any Assessment of Compliance which has been carried out

- any evidence relevant to that assessment

- in cases where an Assessment of Compliance is not provided, the reasons why it is not provided

- any information that the public authority failed to enter in the subsidy database[footnote 77]

- any other information which the Secretary of State specifies by regulations that must be provided[footnote 78]

The information which the Secretary of State has directed the public authority to provide to the SAU must be provided within an ‘information period’ of 20 working days, beginning on the day that the direction is given.[footnote 79]

The SAU must publish its report [footnote 80] within a reporting period of 30 working days, beginning on the earlier of the date on which the information required under the Secretary of State’s direction is provided to the SAU and the day after the information period ends.[footnote 81] A copy of the report will be given to the public authority and the Secretary of State as soon as reasonably practicable following publication.[footnote 82]

The reporting period may be extended if agreed in writing between the SAU and the public authority in question.[footnote 83] The reporting period may also be extended by the Secretary of State in response to a request from the SAU, in line with the procedure outlined above (visit Mandatory referal section) in relation to extensions in the case of mandatory referral.[footnote 84]

Before the end of the reporting period, the SAU will publish its report. The report will include an evaluation of the public authority’s Assessment of Compliance. It will also take into account any effects of the proposed subsidy or scheme on competition or investment within the United Kingdom. If such an assessment has not been carried out, this will be stated in the report. If the subsidy or scheme is ongoing, the report may also include advice about how the subsidy or scheme might be modified to ensure compliance with the Subsidy Control Requirements.[footnote 85]

Exemptions from referral

Referral is not required in relation to:

- subsidies given under a subsidy scheme[footnote 86]

- streamlined subsidy schemes[footnote 87]

- minimal financial assistance[footnote 88]

- ‘SPEI assistance’ as defined in the Act[footnote 89]

- subsidies and schemes which are made exempt from the Subsidy Control Requirements as set out above in Exempt Subidies[footnote 90] (except subsidies in relation to nuclear energy and that the exemption in relation to financial stability directions[footnote 91] only applies in relation to a subsidy or subsidy scheme to which a ‘financial stability direction’ applies or which is otherwise given or made by the Treasury or the Bank of England (or both acting jointly) for ‘prudential reasons’[footnote 92]).

Monitoring

The SAU will monitor and review the effectiveness of the operation of the Act and its impact on competition and investment within the United Kingdom.[footnote 93] Reviews must be carried out in relation to the following periods:

- the first review relates to the period between commencement[footnote 94] and 31 March on the third year following the year of commencement

- the second review relates to the following period of three years

- further reviews will relate to each subsequent period of five years (although the timing of this five-year cycle may be altered as a consequence of the Secretary of State directing the SAU to prepare a report in relation to a ‘specified period’)[footnote 95]

A report must be prepared on the outcome of each review.[footnote 96] The report will be published in a manner the SAU considers to be appropriate, as soon as practicable after the end of the period to which it relates,[footnote 97] and each report will be laid before Parliament.[footnote 98]

For the SAU to prepare a report which reflects accurately the effectiveness of the operation of the Act, it will be necessary to draw on information which the SAU would not otherwise have available to it through its referral function. For that reason, it is important that parties respond as fully and as expeditiously as possible to any information requests they might receive from the SAU in exercising this function. As explained in more detail in the following section, the SAU will have certain information-gathering powers to support it in carrying out this function.

In addition to the SAU’s periodic report on the operation of the subsidy control regime, the SAU’s annual report must also include details of the subsidies and schemes in respect of which the SAU has prepared a report following mandatory, voluntary or post-award referral during the relevant financial year.[footnote 99]

Information-gathering powers

To carry out its functions under the Act, the SAU may need to gather information from public authorities, as well as from other stakeholders such as businesses and/or individuals. In practice, the SAU may seek to obtain such information through informal requests, or by inviting relevant parties to attend meetings or phone calls.

However, in carrying out its monitoring function (as described in the previous section), the SAU will have certain information-gathering powers, enforcement powers and powers to issue penalties.

More specifically, the SAU will have the power to issue a notice requiring a person to provide information or documents, for the purposes of assisting it in carrying out its monitoring and reporting function. The notice, sent in writing, may require:

- any person to produce documents which are in their custody or control, as specified in the notice[footnote 100]

- any person who carries on a business to provide any information as specified or described in the notice[footnote 101]

The person to whom any such document is produced in accordance with a notice may copy the document.[footnote 102]

Before the SAU uses these information gathering powers it will have due regard to the impact of any such request on businesses, public authorities, or individuals.

The SAU may impose a penalty if it considers that a person has, without reasonable excuse, failed to comply with any requirement of a notice or has intentionally obstructed or delayed any person in the exercise of its right to copy any document produced.[footnote 103] The SAU has prepared a statement of policy in relation to the enforcement of such notices[footnote 104]and it will have regard to such statement of policy in deciding whether and, if so, how to exercise its power to impose a penalty.[footnote 105]

Other than as modified by the Act,[footnote 106] the SAU’s information gathering powers will be identical to the powers of the Office of the Internal Market under UK Internal Market Act 2020 (UKIM Act).[footnote 107] However, the Secretary of State may by regulation make provision for such further modifications as are necessary for the purpose of applying the relevant provisions in this context.[footnote 108] Certain modifications will be made by regulation prior to the commencement of the Act.

Procedural arrangements

Introduction

This chapter sets out the procedures the SAU will adopt in carrying out its review functions.[footnote 109] It explains:

- how public authorities should request reports from the SAU

- the steps the SAU expects to take in evaluating the public authority’s assessment

- how the SAU will produce its reports

It addresses the SAU’s review processes covering:

- pre-referral engagement

- how a public authority can request a report through the Public Authority Portal (PAP)

- what the public authority needs to provide with its request, including by way of its Assessment of Compliance and supporting evidence

- our assessment stages including our approaches to transparency, consultation and confidentiality, extensions, the publication of our reports and subsequent cooling off periods

The chapter also considers the SAU’s procedural arrangements for its monitoring and reporting function.[footnote 110]

Referrals of Subsidies and Schemes

This chapter first considers the SAU’s review functions leading to its reports (visit Reports on referal section).

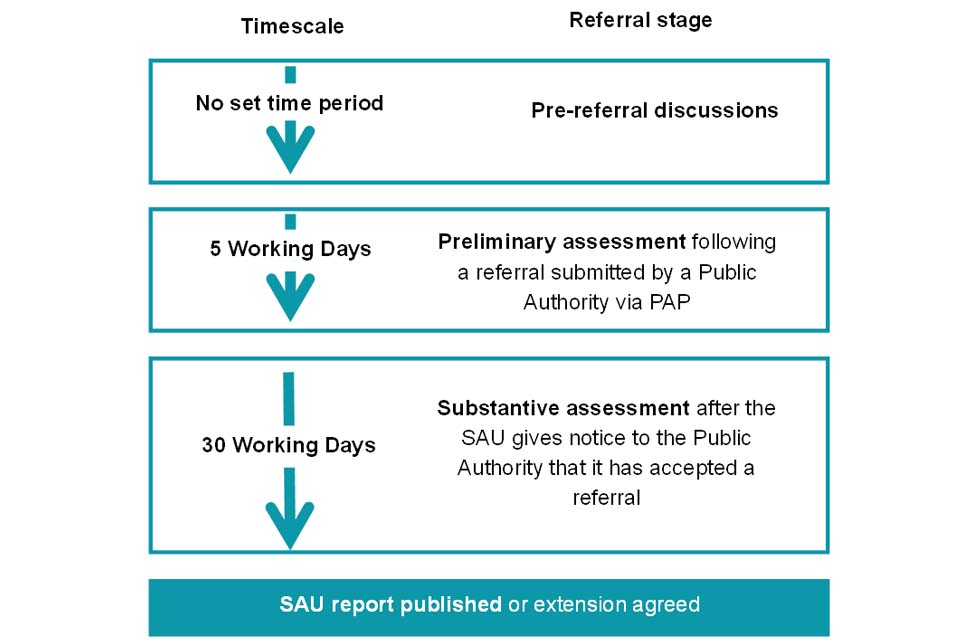

Figure 1 provides an overview of the referral process.

""

Figure 1 description: A diagram showing the timescales involved in the referral process. For pre-referral discussions, there is no set time period. A preliminary assessment following a referral submitted by a Public Authority via the Public Authority Portal must be completed within 5 working days. A substantive assessment after the SAU gives notice to the Public Authority that it has accepted a referral must be completed within 30 working days. The SAU report is then published, or an extension is agreed.

Pre-referral discussions

In order to assist public authorities in preparing a request for a mandatory and voluntary referral to the SAU, the SAU will engage in pre-referral discussions to assist the public authority. The SAU will support the public authority to identify the information that should be submitted when the subsidy or scheme is formally referred. Successful pre-referral discussions should reduce the risk that the SAU will reject the request as incomplete, and ensure the SAU is provided with the information it needs to evaluate the public authority’s assessment.

As well as helping public authorities to prepare their request for a report, pre-referral discussions may cover the SAU’s processes and, for voluntary referrals, the application of its Prioritisation Principles. The discussions are an opportunity for a public authority to explain the proposed subsidy or scheme and its compliance assessment, which will help the SAU familiarise itself with the issues and progress the referral more efficiently. Early discussions will also allow the SAU to plan its evaluation and to make initial preparations.

During pre-referral discussions, the SAU is not able to advise the public authority on the design of subsidies and schemes in compliance with the Subsidy Control Requirements, whether measures qualify as a subsidy, or meet the criteria for referral. Nor will it be able to advise on how a public authority should undertake its Assessment of Compliance. As explained above (visit The Subsidy Advice Unit’s functions, this is not a role of the SAU and we will not be able to offer advice on these matters. The approach to these matters is set out in BEIS Statutory Guidance, which also points to relevant sources of guidance and support.[footnote 111] Pre-referral discussions are not a substitute for public authorities making their own assessment or taking appropriate advice.

Pre-referral discussions are a voluntary step. It is for the public authority to decide when it will submit its request for a report and so trigger the statutory timeframes shown in Figure 1. However, the SAU encourages public authorities to approach it for discussion before referring any subsidies that may meet the definition of SSoI or SSoPI, especially for measures which are complex or novel in nature. As preparing a submission to the SAU is likely to be a significant task, we suggest the public authority contacts the SAU in good time in advance of an anticipated request once their Assessment of Compliance is sufficiently developed. The SAU would welcome discussion at an early stage about appropriate timings, depending on the specific circumstances of the proposed subsidy or scheme. In any event, public authorities are also encouraged to keep the SAU informed of their progress in developing the subsidy or scheme and their expectations of when, or if, a request for review might be made. The SAU will not normally make any public statement about pre-referral discussions on a subsidy.

Where a public authority wishes to discuss the preparation of a referral application with the SAU, it may contact us at [email protected].

Requests for a report

Public authorities should submit their request for a report before the subsidy is given, or the scheme is made, or, in case of a post-award referral, should submit the required information (visit Post-award referral section). This request must be made through the SAU’s Public Authority Portal. This portal is a dedicated secure, auditable communication channel between the SAU and public authorities.[footnote 112], [footnote 113]

It is the public authority’s responsibility to submit the required documents and relevant evidence. To allow the SAU to carry out its evaluation as effectively and efficiently as possible, information should be submitted in a form where the SAU can readily understand the public authority’s assessment and the reasons and evidence for that assessment. All documents should be submitted in a readable and searchable format,[footnote 114] where confidential information is clearly identified (visit Identifying Confidential Information section).

The public authority’s determination of how the measure meets the definition of SSoPI or SSoI and the Assessment of Compliance with the Subsidy Control Requirements should be provided as two separate self-contained documents, where the approach to assessment takes full account of BEIS Statutory Guidance[footnote 115] and any applicable BEIS template, as well as the SAU guidance.

The Assessment of Compliance should clearly identify:

- where in the assessment each of the Principles (and, when applicable, the E&E Principles) are assessed

- which evidence documents are relevant to each part of the assessment

The public authority may additionally provide a description of the process that it followed in gathering relevant evidence and conducting the assessment, explain how the assessment was conducted, and/or may include further explanation of why the public authority reached its conclusions in its assessment.

As part of the evidence relevant to the assessment of compliance with the Subsidy Control Requirements, the public authority should submit any relevant materials that may assist the SAU in evaluating the public authority’s assessment. Among other things, the following documents may be relevant: the subsidy documents describing the subsidy or scheme to potential recipients; a copy of the grant, loan, or guarantee agreement; and any documents describing how applications for a scheme will be assessed. These documents should be sufficiently detailed to allow the SAU to conduct a meaningful evaluation of the public authority’s assessment. Some examples of underlying evidence and analysis that may be relevant are identified in Substantive evaluation of assessment against the Principles, but this is not intended to be a complete list of documents that may be relevant.

The submission should include an index of documents submitted as set out in Appendix A, and it should identify any confidential material (visit Identifying Confidential Information).

Preliminary assessment

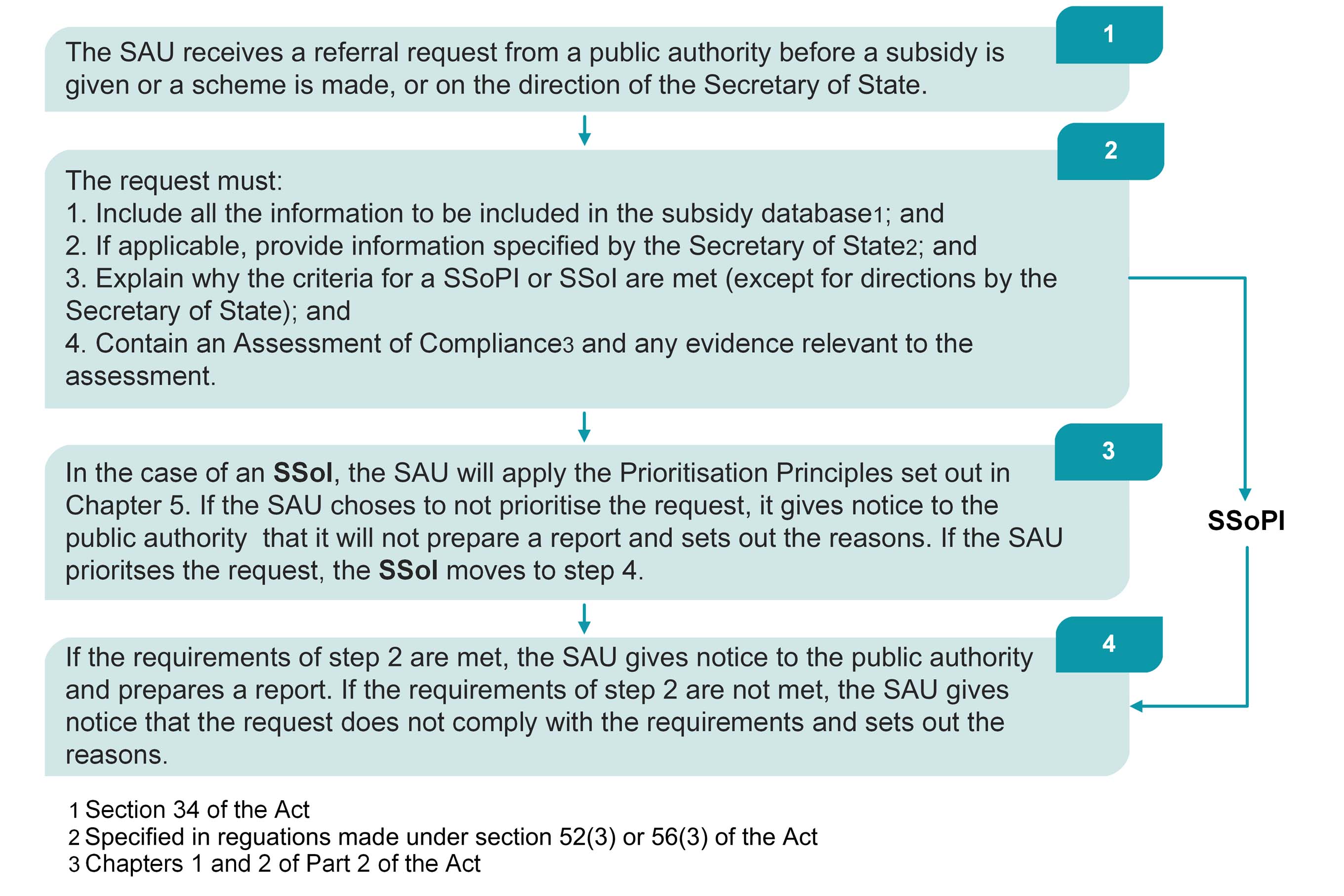

As explained in Chapter 2, upon receipt of a mandatory or voluntary referral request, the SAU has five working days, beginning with the day on which a request is received, to undertake a preliminary assessment to decide whether it will provide a report. In undertaking that preliminary assessment, the SAU will use the process map shown in Figure 2 for considering whether a subsidy Assessment of Compliance meets the requirements for a referral.[footnote 116]

""

Figure 2 description: Process map for Preliminary Assessment for considering whether a subsidy Assessment of Compliance meets the requirements for referral.

Step 1. The SAU receives a referral request from a public authority before a subsidy is given or a scheme is made, or on the direction of the Secretary of State.

Step 2. The request must: firstly, include all the information to be included in the subsidy database under Section 34 of the Act; and secondly, if applicable, provide information specified by the Secretary of State, specified in regulations made under section 52(3) or 56(3) of the Act; and thirdly, explain why the criteria for a SSoPI or SSoI are met (except for directions by the Secretary of State); and fourthly, contain an Assessment of Compliance and any evidence relevant to the assessment, under Chapters 1 and 2 of Part 2 of the Act.

Step 3. In the case of an SSoI, the SAU will apply the Prioritisation Principles set out in Chapter 5 of the SAU’s guidance. If the SAU choses to not prioritise the request, it gives notice to the public authority that it will not prepare a report and sets out the reasons. If the SAU prioritises the request, the SSoI moves to step 4. SSoPI requests skip step 3 of the process and proceed from step 2 to step 4.

Step 4. If all the requirements of step 2 are met, the SAU gives notice to the public authority and prepares a report. If the requirements of step 2 are not met, the SAU gives notice that the request does not comply with the requirements and sets out the reasons.

The reporting period and transparency

The 30-working day reporting period starts on the day on which the SAU notifies the public authority that it has accepted the referral.

As soon as practicable after such notice has been issued, and generally within the first five working days after acceptance of the referral, the SAU will publish information on the referral on its website to help ensure the transparency of the SAU’s review. Transparency is a fundamental part of the UK’s subsidy control regime, promoting the accountability and challenge that is expected to result in better subsidy design and improved decisions.

Published information is likely to include the information that would be entered in the subsidy database,[footnote 117] which the public authority is required to submit in its request.[footnote 118] Where necessary to the understanding of the proposed subsidy or scheme, we may ask the public authority to provide an appropriate non-confidential description and provide links to published announcements of the subsidy or scheme, to be included in the information the SAU will publish. The SAU will generally not accept representations that it is not possible to publish a high-level description during the early stages of the referral because of the confidentiality of the policy aim, in particular given that our reports must be published only a short time afterwards.

Third parties will have the opportunity to make relevant representations. For example, third parties might identify factors, such as alternative ways the authority could have achieved the same aim, or impacts on markets, competition and investment, that would be relevant to the Assessment of Compliance and would not otherwise be brought to the SAU’s attention.

The SAU may take account of third-party submissions, insofar as they are relevant to the evaluation of the public authorities’ assessment, and provided they are submitted within a short time-period specified by the SAU. This will typically be limited to 10 working days to allow time for the SAU to factor relevant submissions into its evaluation. The SAU will not take account of submissions which are not relevant to the SAU’s statutory functions.

We will not generally publish third party submissions, although the matters raised may be reflected in the SAU’s reports.[footnote 119] We however encourage third parties to share their submission to the SAU with the public authority. In order to properly take account of the outcomes of our report, the public authority, as decision maker on the subsidy, needs to be able to consider all the information and evidence that underpins it, including third party’s views. The SAU will therefore send all third-party submissions to the public authority with the copy of the report. The public authority may need to treat these submissions as confidential as third parties may have indicated information is sensitive (visit Identifying Confidential Information). Any submissions from third parties should therefore include an express consent for it to be shared with the public authority. It may be possible to agree to sharing an anonymised version of the submission. Submissions that cannot be shared with the public authority will not be considered in our reports.

The SAU will primarily base its evaluation on the information in the public authority’s referral request. Public authorities will not routinely be able to refine or clarify information after the submission of their request, although the SAU may on occasion ask the public authorities for clarification where necessary. If necessary, we may request clarification from the public authority to check our understanding of the submissions. The SAU may also approach relevant regulators and similar public bodies for information where appropriate and, exceptionally, other relevant third parties, including participants in the relevant market(s).

Should the SAU consider that proactive engagement is necessary, it will endeavour to start engagement within the first 15 working days of the review period.

Use of CMA groups

The governance of referrals will be done through a committee of the CMA Board, the SAU Committee. However, the SAU may make a reference to a specially constituted independent CMA group.[footnote 120] The use of CMA group is likely to be exceptional and dependent on an extension being agreed, where the SAU decides it is appropriate in the circumstances.

Extensions to the reporting period

As set out in Reports on referral, the reporting period may be extended by agreement between the SAU and the public authority,[footnote 121] or, for mandatory referrals and post-award referrals, at the direction of the Secretary of State following a request from the SAU, and where justified by exceptional circumstances.[footnote 122]

The SAU will typically first seek to agree any extension with the public authority. It may request one from the Secretary of State if it has been unable to reach an agreement. Any such request will be published on the SAU’s website.[footnote 123]

Where an extension is agreed between the SAU and the public authority, the SAU will publish on its website a notice explaining that the reporting period has been extended and the reasons for the extension. Such reasons might include, among others, the complexity or volume of the documentation provided, the appointment of a CMA group (visitUse of CMA groups), or where issues arise during the reporting period which require further time to address.

Publication and confidentiality

The SAU will publish its report on its website before the end of the reporting period and will aim to provide a copy of the report to the relevant Public Authority and the Secretary of State as soon as reasonably practicable after its publication.[footnote 124] Where possible and practicable shortly before publication, we will communicate orally to the public authority the outcome of our evaluation, on a strictly embargoed basis. This will enable the public authority to prepare to prepare its external and/or internal communications.

Identifying Confidential Information

The CMA is under statutory obligations to protect the confidentiality of information relating to individuals and businesses where that information comes to it in connection with the exercise of its statutory functions. That will include information relating to individuals and businesses provided to the SAU by public authorities. This section sets out more generally how the SAU will handle confidential information.

To limit the need to redact confidential information and therefore maximise transparency, the SAU’s reports will, where possible, be drafted without reference to confidential information, provided that does not undermine the clarity and accuracy of its reports. This will help ensure that all public authorities and others can understand our evaluation and help share best practice.

To facilitate this process, public authorities should clearly identify confidential information in their submissions, including any third-party confidential information. In each case, the submission must include sufficient explanation for the claim, including the nature, magnitude and likelihood of any harm that may be caused by its disclosure, and for third party confidential information, an indication of its source and the circumstances in which it was obtained. It is not sufficient simply to mark a referral, or whole documents, ‘confidential’ or ‘OFFICIAL SENSITIVE COMMERCIAL’ without further explanation. As noted in The reporting period and transparency section, we would expect to publish a short description of the proposed subsidy or scheme on our website early in the referral period, and further details will be incorporated within our report where relevant to our evaluation.

Any third parties submitting information directly to the SAU in accordance with The reporting period and transparency section of this guidance must likewise identify any confidential information and provide an explanation in the same manner. We will take account of this in developing our published report. As noted, third party submissions will be shared in full with the public authority when we publish our report.

When identifying information as confidential, public authorities and third parties should have regard to the CMA’s guidance on transparency and disclosure and to the information under the Enterprise Act 2002 (EA02).[footnote 125]

Public authorities should not withhold information from the SAU on grounds of confidentiality. The Act requires public authorities to include any evidence relevant to their assessment.[footnote 126] If the relevant public authority has information which it considers confidential but which is relevant to its assessment, it should provide that information suitably identified as confidential, as set out in this section.[footnote 127] The SAU will take into account whether relevant confidential information has been withheld when deciding whether a request for a report complies with the requirements of the Act.

Handling of confidential information

The SAU is under statutory obligations to protect confidential information. In particular, the SAU is under a general restriction on the disclosure to other persons of certain information relating to individuals and businesses obtained during the exercise of its statutory functions (referred to as ‘specified information’). It may only disclose such information where permitted by statute, including for the purpose of facilitating the exercise of its statutory functions.[footnote 128] Where disclosure of these categories of specified information is permitted, the SAU must also have regard to the three additional considerations:[footnote 129]

- the need to exclude from disclosure (so far as is practicable to do so) any information whose disclosure is considered to be contrary to the public interest

- the need to exclude from disclosure (so far as practicable) commercial information which might significantly harm the legitimate business interests of the undertakings or information relating to the private affairs of an individual which might significantly harm that individual’s interests

- the extent to which the disclosure of information relating to the private affairs of an individual or commercial information is necessary for the purpose for which the authority is permitted to make the disclosure

The SAU will apply these considerations on a case-by-case basis. For example, we will consider the extent to which disclosure is necessary to allow other public authorities to understand the reasons for our evaluation in order to ensure that best practice is spread and that public authorities can more effectively design compliant subsidies and schemes.

If the SAU considers that it needs to disclose information which has been identified as confidential, it will inform the relevant public authority or third party, setting out the reasons why it believes it is necessary. The relevant public authority or third party will then be able to make representations as to why the information should not be disclosed, including expanding on the explanations originally provided about why the information is confidential and the potential harm that might arise from publication. The public authority or third party may also wish to consider and propose alternative forms of that information which can be published (for example, ranges in place of specific figures).

The short statutory deadline means that the time available to discuss disclosure will necessarily be limited, and likely come close to the publication deadline. Public authorities and third parties should ensure that they are prepared to respond to any confidentiality matters at short notice. Where a public authority has provided third-party confidential information, the CMA may require the public authority to facilitate correspondence with any affected third party.

The SAU will consider any representations received and will ultimately decide whether to disclose the information. If the relevant public authority or third party still does not agree with the approach to disclosure of confidential information taken by the SAU, it can apply to the CMA’s Procedural Officer.[footnote 130]

In exceptional circumstances (e.g. where time is critical), the SAU may choose to publish a redacted version of the report, which it may then amend once agreement over the inclusion of confidential information has been reached.

Further information on the CMA’s obligations regarding the protection and disclosure of information under the EA02, Competition Act 1998 (CA98) and the Freedom of Information Act 2000 (FOIA), which also apply to the function of the SAU, is set out in Transparency and Disclosure: Statement of the CMA’s policy and approach (CMA6).

The CMA handles personal data within the meaning of the UK GDPR and the Data Protection Act 2018 in accordance with its privacy policy.[footnote 131] The Act does not permit or require disclosure of information in contravention of data protection legislation.[footnote 132]

Monitoring report and information gathering procedure

Chapter 4 sets out the analytical approach to the monitoring and reporting functions.[footnote 133] The SAU has information gathering powers for the purpose of carrying out this function.[footnote 134] Further detail is provided below and will be provided in the Statement of Policy on the Enforcement of the SAU’s Information Gathering Powers.[footnote 135]

The SAU will, where appropriate, send out formal information requests (‘section 41 notices’) in writing to obtain information from businesses, public authorities, or individuals.

Under this power, the SAU may ask for information or documents under the person’s custody or control, as well as information that is not already written down. The SAU may also require explanation of any document that is produced.

The SAU’s section 41 notices will set out their purpose, specify or describe the documents and/or information that the SAU requires, give details of where and when they must be produced and set out the consequences, if any, that may apply if the recipient does not comply. The SAU will seek to set a reasonable deadline for all information requests and take into account comments from recipients on the requests. Section 41 notice addressees should contact the SAU as soon as possible after receiving a request and make known any difficulty in responding – for instance, given the nature of the information requested, or the resources available to them. The SAU will discuss any queries raised by addressees including any difficulty in submitting the information in the requested format or within the requested timeframe.

Analytical framework

Reports on Referral

Introduction

This section explains how the SAU will analyse the public authority’s assessment of the subsidy or subsidy scheme’s compliance with the Subsidy Control Requirements. This section contains an outline of:

- the substantive 30-day evaluation of the public authority’s assessment

- the content of the SAU’s report

Substantive evaluation of assessment against the Principles

This chapter will refer to the Principles:

Principle A: Common interest

Subsidies should pursue a specific policy objective in order to:

- remedy an identified market failure, or

- address an equity rationale (such as local or regional disadvantage, social difficulties or distributional concerns)

Principle B: Proportionate and necessary

Subsidies should be proportionate to their specific policy objective and limited to what is necessary to achieve it.

Principle C: Design to change economic behaviour of beneficiary

- Subsidies should be designed to bring about a change of economic behaviour of the beneficiary.

- That change, in relation to a subsidy, should be

- conducive to achieving its specific policy objective, and

- something that would not happen without the subsidy

Principle D: Costs that would be funded anyway

Subsidies should not normally compensate for the costs the beneficiary would have funded in the absence of any subsidy.

Principle E: Least distortive means of achieving policy objective

Subsidies should be an appropriate policy instrument for achieving their specific policy objective and that objective cannot be achieved through other, less distortive, means.

Principle F: Competition and investment within the United Kingdom

Subsidies should be designed to achieve their specific policy objective while minimising any negative effects on competition or investment within the United Kingdom.

Principle G: Beneficial effects to outweigh negative effects

Subsidies’ beneficial effects (in terms of achieving their specific policy objective) should outweigh any negative effects, including in particular negative effects on: * competition or investment within the United Kingdom * international trade or investment

When preparing Compliance Assessments, public authorities must have regard to BEIS Statutory Guidance.[footnote 136] The SAU’s task is to evaluate the public authority’s assessment, not to carry out its own assessment. Hence the fundamental questions that the SAU will consider are:

- How well does the public authority’s assessment address the subsidy’s compliance with the Subsidy Control Requirements?

- Has appropriate relevant evidence been identified and used in the assessment, and are the public authority’s analysis and conclusions generally consistent with that evidence?[footnote 137]

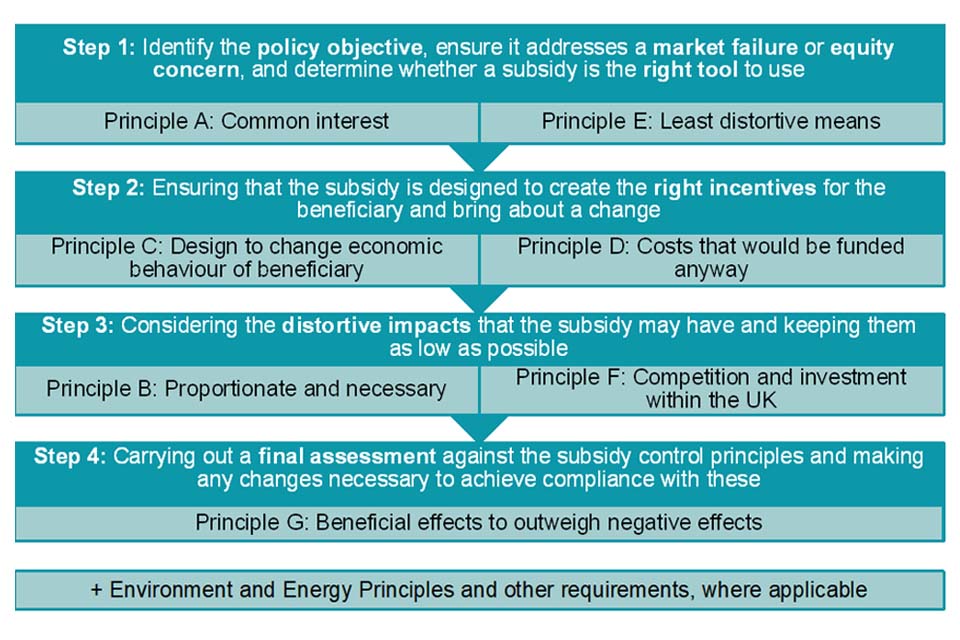

The SAU’s evaluation must take into account any effects of the proposed subsidy on competition or investment within the UK.[footnote 138] This section of the guidance sets out the framework that the SAU will use to conduct its evaluation of the public authority’s Assessment of Compliance. This framework is based on the 4-step assessment framework set out in BEIS Statutory Guidance.[footnote 139]

The steps in the 4-step framework are:

-

identifying the policy objective, ensuring it addresses a market failure or equity concern, and determining whether a subsidy is the right tool to use

-

ensuring that the subsidy is designed to create the right incentives for the beneficiary and bring about a change

-

considering the distortive impacts that the subsidy may have and keeping them as low as possible

-

carrying out a final assessment against the subsidy control principles and making any changes necessary to achieve compliance with these

For each of the steps in the BEIS 4-step framework, we identify below broadly how each corresponds to the 7 subsidy control principles. See also the corresponding diagram at Appendix B.

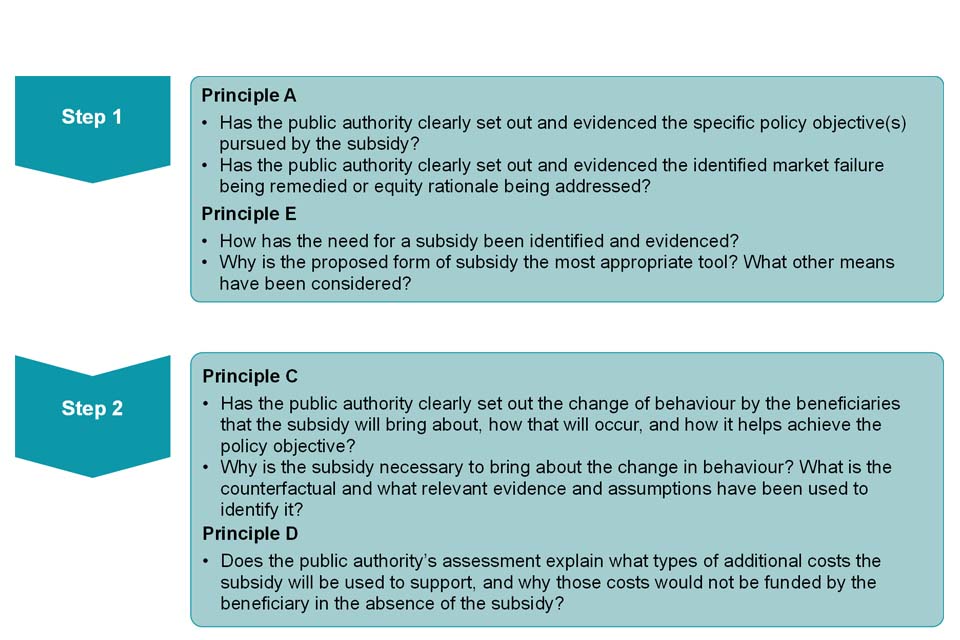

Step 1: Identifying the policy objective, ensuring it addresses a market failure or equity concern, and determining whether a subsidy is the right tool to use

The public authority’s assessment should address compliance with the requirements of Principles A and E.[footnote 140]

The SAU evaluation is not intended to impinge on public authorities’ discretion to define their own policy objectives, but will evaluate how the objective has been set out and what supporting evidence has been provided.

The SAU’s report will consider how the public authority’s assessment demonstrates that the proposed subsidy targets the policy objective, in the most appropriate and least distortive way. Public authorities should clearly articulate in the rest of the assessment how the subsidy will achieve the policy objective identified.

The SAU’s evaluation of the public authority’s assessment will consider the following:

Principle A: Common interest

- Has the public authority clearly set out and evidenced the specific policy objective(s) pursued by the subsidy?

- Has the public authority clearly set out and evidenced the identified market failure being remedied or equity rationale being addressed?

Principle E: Least distortive means of achieving policy objective

- How has the need for a subsidy been identified and evidenced?

- Why is the proposed form of subsidy the most appropriate tool? What other means have been considered?

Supporting evidence relevant to these points may include:

- the public authority’s business case, value for money assessment, and/or equivalent policy appraisal and/or cost-benefit analysis

- technical reports commissioned or undertaken to support the public authority’s analysis

- evaluations of similar previous subsidies or schemes, and/or alternative options considered

- output from any public or industry consultation exercises

Step 2: Ensuring that the subsidy is designed to create the right incentives for the beneficiary and bring about a change

The public authority’s assessment should address compliance with the requirements of Principles C and D.[footnote 141]

The SAU’s evaluation of the public authority’s assessment will consider the following:

Principle C: Design to change economic behaviour of beneficiary

- Has the public authority clearly set out the change of behaviour by the beneficiaries that the subsidy will bring about, how that will occur, and how it helps achieve the policy objective?

- Why is the subsidy necessary to bring about the change in behaviour? What is the counterfactual and what relevant evidence and assumptions have been used to identify it?

Principle D: Costs that would be funded anyway

- Does the public authority’s assessment explain what types of additional costs the subsidy will be used to support, and why those costs would not be funded by the beneficiary in the absence of the subsidy?

Supporting evidence relevant to these points may include:

- the public authority’s business case, value for money assessment, and/or equivalent

- relevant commercial and/or financial analysis or documents prepared or commissioned by the beneficiary (e.g. business plans and budgets; profitability calculations for a given project with and without subsidy; project finance analysis; risk assessments; counterfactual analysis)

- any draft subsidy agreement or scheme terms (the assessment should highlight provisions relevant to the assessment – for example conditions set out in the subsidy agreement or scheme stipulating how the subsidy can be used, including how these will be monitored and enforced)

- any additional counterfactual analysis prepared as part of the public authority’s policy appraisal

Step 3: Considering the distortive impacts that the subsidy may have and keeping them as low as possible

The public authority’s assessment should address compliance with the requirements of Principles B and F.[footnote 142]

The SAU’s evaluation of the public authority’s assessment will consider the following:

Principle B: Proportionate and necessary

- How does the public authority’s assessment demonstrate that the subsidy is proportionate to the specific policy objective?

- How does the public authority’s assessment demonstrate that the subsidy is limited to the minimum needed to induce the relevant investment or activity?

Principle F: Competition and investment within the UK

- How does the public authority’s assessment address ways in which the design of the subsidy minimises any negative effects on competition or investment within the UK? For example:

- is the subsidy available to a broad set of recipients, rather than a narrow set or an individual enterprise? What criteria were used or are proposed for selecting beneficiaries?

- how is the subsidy targeted towards the specific policy objective (rather than supporting beneficiaries’ wider activities)? Does it include performance criteria and dispute mechanisms, including clawback provisions?

- the nature of the subsidy (e.g. loan rather than grant) and its impact on costs (e.g. lump-sum payment, variable (per unit) payment, tax reduction)

- the timespan over which a subsidy is provided

Supporting evidence relevant to these points may include:

- the public authority’s business case, value for money assessment, and/or equivalent

- any draft subsidy agreement or scheme terms (the assessment should highlight provisions relevant to the assessment - for example conditions set out in the subsidy agreement or scheme stipulating how the subsidy can be used, including how these will be monitored and enforced)

- relevant commercial and/or financial analysis and/or documents prepared or commissioned by the beneficiary (e.g. on the required amount of subsidy)

- for subsidies for rescuing or restructuring an ailing or insolvent enterprise, details of the beneficiary’s financial position

Effects on UK competition or investment, or international trade or investment

Consideration of the effects of a subsidy on UK competition or investment, or international trade or investment, is relevant to the assessment of compliance with both Principle F and Principle G. The SAU’s evaluation of the public authority’s assessment will consider the following:

- has the public authority conducted an appropriate analysis to identify the product markets (and key related markets) likely to be affected by the subsidy, and provided any relevant evidence in support of this?

- has the public authority conducted an appropriate analysis to identify the geographic scope of affected markets, and provided any relevant evidence in support of this?

- how does the public authority expect the subsidy to affect the behaviour of recipients?

- given the characteristics of the subsidy, and the characteristics of the market(s), how has the public authority assessed potential effects this may have on:

- current and potential competitors

- suppliers and customers

- entry conditions and incentives

- innovation incentives

- UK investment

- international trade or investment

Supporting evidence relevant to these points may include:

- assessment of the parties, products and markets affected by the subsidy

- market research reports used in identifying relevant markets and market characteristics

- published reports or decisions by competition or regulatory authorities relating to relevant markets (or similar markets)

- the public authority’s business case, or equivalent policy appraisal or cost-benefit analysis

- output from any public or industry consultation exercises

Step 4: Carrying out a final assessment against the subsidy control principles and making any changes necessary to achieve compliance with these

The public authority’s assessment should address compliance with the requirements of Principle G.[footnote 143]

The SAU’s evaluation of the public authority’s assessment will consider the following:

Principle G: Beneficial effects to outweigh negative effects

- how has the public authority evaluated and measured:

- expected beneficial effects of the subsidy (in terms of achieving their specific policy objectives)

- potential negative effects of the subsidy on competition or investment within the UK and/or international trade or investment.

- how have geographical and distributional impacts within the UK been assessed?

- how has the public authority approached balancing the beneficial effects of the subsidy against any negative effects?

Supporting evidence relevant to these points may include:

- the public authority’s business case, or equivalent policy appraisal or cost-benefit analysis

- output from any public or industry consultation exercises.

E&E Principles

Where relevant, the SAU will also evaluate the public authority’s assessment of whether the subsidy or scheme would comply with the E&E Principles (and any evidence relevant to that assessment).[footnote 144]

Prohibitions and other requirements

Where relevant, the SAU will also evaluate the public authority’s assessment of the subsidy or scheme’s compliance with the prohibitions and other requirements of the Act (and any evidence provided relevant to that assessment).[footnote 145]

Submissions from third parties

The SAU’s role is to evaluate the public authority’s assessment as submitted along with relevant evidence. It is the public authority’s responsibility to collect evidence relevant to its assessment, including representations from third parties (such as subsidy recipient(s), their (potential) competitors, customers, etc.). Where interested third parties make submissions to the SAU, the SAU may consider them in the context of its evaluation of the public authority’s assessment, and may reflect them in its report.[footnote 146]

The SAU’s report

The SAU’s evaluation of the public authority’s assessment will be included in the SAU report.[footnote 147]

The SAU will aim to ensure that its reports are clear and concise. The SAU’s report will not take the form of a ‘pass/fail’ evaluation, but will identify any shortcomings in the public authority’s assessment (or evidence base), and may identify where the assessment is strong.

The report may also include:

- advice about how the public authority’s assessment might be improved

- advice about how the proposed subsidy or scheme may be modified to ensure compliance with the requirements of the Act

Where applicable, the SAU will comply with any regulations made by the Secretary of State as to content or form[footnote 148]. Notwithstanding this, the SAU may decide the form and content of the report it provides. The substantive evaluation in the report will generally follow the structure of the principles analysis in the Analytical Framework of this Guidance.

Monitoring report

As set out in Chapter 2, the SAU must monitor and review the effectiveness of the operation of the Act and its impact on competition and investment within the United Kingdom.[footnote 149] The SAU must prepare a report on the outcome of its review and publish it as soon as practicable after the end of the relevant review period (visit Monitoring for details on the review periods).

The review will consider the effectiveness of the Act and regime as a whole (rather than just those subsides whose assessment has been evaluated by the SAU). Among other things, the review may include consideration of:

- the effectiveness of the subsidy control principles in meeting the aims of the regime and how they are applied

- prohibitions and requirements on subsidies

- the general understanding of the regime by public authorities, including the effectiveness of their assessments

- whether thresholds (e.g. for SSoIs and SSoPIs) continue to be set appropriately

- the effectiveness of the SAU’s evaluations

- the operation and impact of the subsidy database

- the extent and impact of legal challenges to the CAT and international agencies

- whether the subsidy regime is facilitating the effective delivery of benefits to the UK economy (including investment)

- whether the costs and benefits of the regime are in proportion and how they are distributed across the United Kingdom, across sectors of the economy and different groups of the population and its impact on competition, investment and trade

The review will consider the views of relevant stakeholders along with a range of evidence, and the report may present and provide commentary on this evidence to provide an overview of how well the Act is operating across the UK. Evidence that we may consider will include (but not be limited to):

- information collected through our monitoring tools

- data gathered by others (including the subsidy database)

- any findings from SAU-commissioned research (including surveys)

- targeted and general stakeholder engagement (including through the use of our information gathering powers (visit Information-gathering powers)

Prioritisation principles

The SAU will review SSoPIs that are referred by public authorities and any subsidy that is called in or referred on a post-award basis by the Secretary of State. The SAU will not have discretion in deciding whether to review these subsidies.

However, the SAU will have discretion in deciding whether to prepare a report in respect of any SSoIs referred by public authorities on a voluntary basis. The SAU needs to ensure it takes appropriate decisions about the types of SSoIs on which it decides to focus its resources. The SAU’s decisions in this regard will be informed by the Prioritisation Principles set out in this chapter.

These principles take the need for swift decision-making into account – although, as detailed in Pre-referral discussions, we strongly encourage public authorities to engage with the SAU before referring a SSoI.

This approach to prioritisation will evolve with experience. The factors listed under each principle are illustrative and not exhaustive and will be limited by the information provided by the public authority as part of its request. The principles will not be applied in a mechanistic way. The SAU will consider the principles in the round and on a case-by-case basis, and may base its decisions on any one or combination of the principles. Where appropriate, we may also take account of other relevant factors.

Principle 1 – Impact

The SAU considers that its review of SSoIs will have the most impact in cases where the subsidy/subsidy scheme has the greatest potential to have a negative effect on competition or investment within the UK, or on international trade and investment.

In considering impact, the SAU will take into account a range of factors that will include:

- subsidy characteristics: monetary value/budget (including relative to size of affected market); timespan; type of financial assistance being provided (e.g., grant, loan, equity stake etc.); any conditions attached to the subsidy; degree of selectivity

- market characteristics: market concentration, and market position(s) of recipient(s) relative to others; geographic scope of subsidy relative to that of market participants

- additional characteristics and design criteria set out in BEIS Statutory Guidance: the SAU is mindful that BEIS Statutory Guidance recommends referral of SSoIs that satisfy the criteria set out in sections 19, 22, 23 of the Act[footnote 150] or which exhibit any design features set out in BEIS Statutory Guidance

Principle 2 – Significance

The SAU will consider the wider strategic significance of reviewing a SSoI. There are a range of factors that the SAU may take into account. This includes, but is not limited to, the following:

- sensitivity: whether a similar subsidy has been subject of a domestic or international challenge or dispute, which may include consideration of the sector to which the subsidy relates.

- balanced programme of work: the SAU will consider how completion of a review might contribute to a programme of work that delivers on behalf of a range of public authorities, including those based in different Nations and regions of the UK, and across sectors.

- contribution to knowledge growth: whether the completion of a review is likely to contribute to public authorities’ and the SAU’s knowledge and understanding of the application of the subsidy control requirements in a particular sector or to a particular category of subsidy (including contribution to the SAU’s wider understanding of the interaction of subsidy control with matters of strategic interest to the CMA as a whole).

- appropriateness: whether the preparation of a report by the SAU is likely to add significant value in assisting the public authority to consider the compliance of a subsidy with the Subsidy Control requirements, or whether there may be other, and more appropriate, means for the public authority to access guidance and support on the subsidy, particularly in more straightforward cases.

- information provision: whether the information submitted in support of the request appears sufficiently detailed to allow the SAU to undertake a review that is likely to result in meaningful findings.

Principle 3 – Resources

The SAU will consider the resource implications of preparing a report in response to any voluntary referral, whilst balancing its mandatory workload.

Glossary

This Glossary explains how certain key terms used in this Guidance can be understood in relation to the SAU functions.

| the Act | The Subsidy Control Act 2022 |

| Assessment of Compliance | The assessment carried out by the public authority as to whether the subsidy or scheme complies with the Subsidy Control Requirements and the reasons for that conclusion |

| BEIS | The Department for Business, Energy and Industrial Strategy |

| BEIS Statutory Guidance | The guidance issued by BEIS under section 79 of the Act on the practical application of certain aspects of the regime. |

| CMA | The Competition and Markets Authority, the body responsible for ensuring that competition and markets work well for consumers |

| Cooling off period | The period after the publication of the SAU’s report which must elapse before the public authority gives the subsidy following a mandatory referral |

| the E&E Principles | The Energy and Environment Principles as set out in Schedule 2 of the Act |

| Mandatory Referral | A referral made under section 52 of the Act, including referrals of SSoPIs and of subsidies called in by the Secretary of State under section 55 of the Act |

| the Principles | The Subsidy Control Principles as set out in Schedule 1 of the Act |

| PAP | The Public Authority Portal, a dedicated, auditable communication channel that will allow 2-way communications between the SAU and public authorities in relation to referrals |

| Post-Award Referral | A referral made under section 60 of the Act by the Secretary of State after a subsidy has been given or a scheme has been made |

| Reporting Period | The period within which the SAU must publish its report on a referral. |

| Subsidy | A subsidy is defined in sections 2-8 of the Act. Further information on the definition of a subsidy can be found in Chapter 2 of BEIS Statutory Guidance. |

| Subsidy Control Requirements | The requirements under Chapters 1 and 2 of Part 2 of the Act, including the obligation to consider whether a subsidy or scheme complies with the Principles (and the E&E Principles, where applicable), as well as the prohibitions and other requirements as set out in Chapter 2 of Part 2t |

| Subsidy Database | The database provided for in Chapter 3 of Part 2 of the Act, on which public authorities are required to enter certain information about subsidies they give or subsidy schemes they make |

| SPEI | Services of public economic interest, as defined in section 29 of the Act |

| SSoI / Subsidies and schemes of Interest | Subsidies and schemes of interest, as defined in regulations made by the Secretary of State under section 11 of the Act |

| SSoPI / Subsidies and schemes of particular interest | Subsidies and schemes of particular interest, as defined in regulations made by the Secretary of State under section 11 of the Act |

| Voluntary Referral | The referral of an SSoI made under section 56 of the Act |

Annex A: Submission of supporting documents in a request for a report

When a public authority submits its request for a report through the public authority portal, all documents should be provided in a suitable format, and must be individually numbered and titled.

The request should include an index of documents submitted which specifies the following:

- document number

- file name

- document title

- purpose of document

- date produced

- produced by (if applicable)

- brief description of its relevance to the assessment (for example as supporting evidence in respect of the evaluation of compliance with subsidy principle x)

The public authority needs to provide a detailed description of whether any parts of the material it has submitted are considered as confidential, and the reasons for this. The descriptions need to be specific to allow us to understand what material, if used in our reports, would raise confidentiality concerns. Because we are required to publish our reports, we cannot accept blanket requests for confidentiality claiming that the entire contents of any or all documents are confidential.

To allow us to understand the Assessment of Compliance, it will need to include:

- details of where in the assessment each of the Principles are assessed

- details of which evidence documents are the ones relevant to the part of the assessment

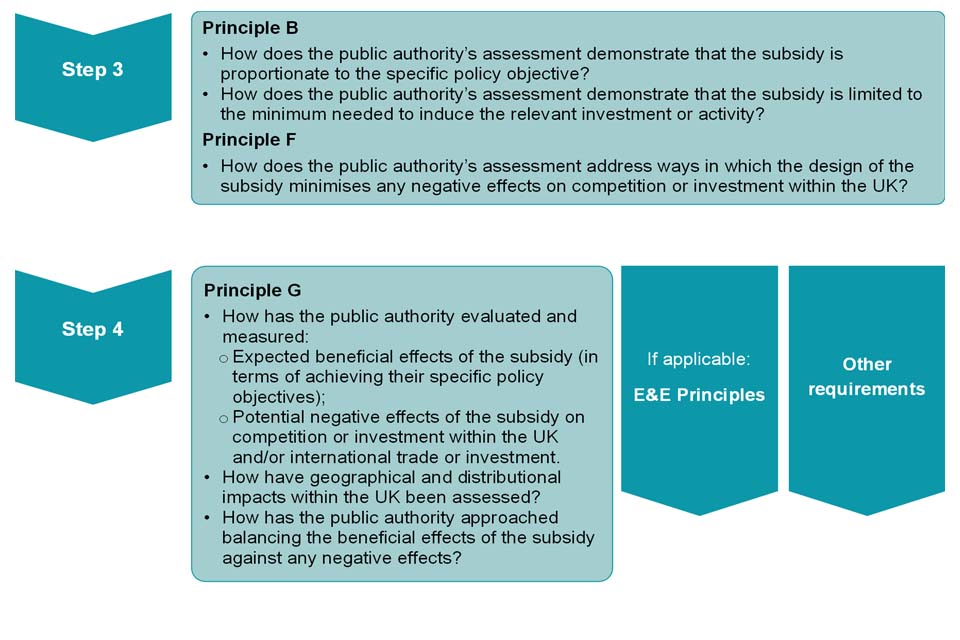

Annex B: 4-Step framework and the Subsidy Control Principles

""

Figure 3 description:

Step 1. Identify the policy objective, ensure it addresses a market failure or equity concern, and determine whether a subsidy is the right tool to use. The principles that relate to step 1 are Principle A: common interest and Principle E: least distortive means.

Step 2. Ensuring that the subsidy is designed to create the right incentives for the beneficiary and bring about a change. The principles that relate to step 2 are Principle C: design to change economic behaviour of beneficiary and Principle D: costs that would be funded anyway.

Step 3. Considering the distortive impacts that the subsidy may have and keeping them as low as possible. The principles that relate to step 3 are Principle B: Proportionate and necessary and Principle F: Competition and investment within the UK.